Beware the Cameron Trap plus other political pratfalls

Beware the Cameron Trap plus other political pratfalls

What caught my eye this week including Labour's unconvincing Brexit reset, the unconservative Tories, why Spain beats France, China's Draghi moment, and saving the planet with debt-for-nature swaps

1. The Cameron Trap

As Sir Keir Starmer prepared to head to Brussels next week for a meeting with Ursula von der Leyen to discuss his plan for a reset of relations between Britain and the European Union, can the prime minister avoid the Cameron trap? In a new piece for The New European, I recall how the former prime minister’s biggest mistake was to publicly announce an EU negotiation without having first established a clear idea of what he wanted and whether he was likely to get it. The result was expectations set too high, leading to disappointment and political humiliation.

In fact, Cameron managed to fall into this trap not once but twice. First when he tried to blackmail the rest of the EU at the height of the eurozone crisis with some preposterous last minute demands cobbled together to appease his party headbangers. Secondly, when he gambled Britain’s EU membership on his ability to deliver reforms to the terms of membership before he even knew what reforms he wanted. Since then a succession of British ministers have tried to negotiate with Brussels convinced that they possess the unique charisma necessary to erase EU red lines.

Whether Starmer has done his homework isn’t clear. I’m sceptical for the reasons I explained before the election. We know what he wants: a security pact, a vetinrary deal, mutual recognition of professional qualifications, and improved touring rights for musicians. We also know some of what the EU wants from Britain: full implementation of the existing Brexit deal, particularly with respect to Northern Ireland, a new fisheries deal, and youth mobility deal that would allow young Europeans and Britons work and study in each other’s countries for a limited time.

But the fact that Starmer appeared to reject the latter out of hand over the summer sent an ominous signal about his preparedness and political antennae. It inevitably highlights what is the biggest concern in Brussels about getting into any new negotiation with London: whether Starmer is prepared to stand up to opposition to any deal from Brexiteers and the right-wing press who can be certain to denounce anything the government agrees with Brussels as a betrayal.

The fact that Starmer has yet to roll the pitch domestically for any concessions to the EU will similarly raise concerns that this reset is just another British cherry-picking exercise. Certainly as this recent paper by the UK in a Changing Europe think-tank points out, any deal that moves the economic dial will be far from straightforward. A veterinary deal will require Britain to align with EU food standards and accept the jurisdiction of the European Court of Justice. In many areas where Britain might want a closer relationship - for example, rejoining the internal energy market, or the emissions trading scheme of the REACH regime for chemicals - the price is likely to be greater participation in EU institutions and paying into the EU budget.

Indeed, as I say in the piece, Starmer’s biggest challenge will be to convince Brussels to reopen a deal that took four ill-tempered years to negotiate but which it believes is working well. The reality is that Britain is far down the EU’s list of priorities:

With a new Commission due to take office in December, the main focus in Brussels is on reviving the EU’s flagging economy, securing its borders, boosting provision for Europe’s defence, preparing for possible enlargement including to Ukraine and managing the clean energy transition. Mario Draghi has just published a 400 page report on how to revive the EU’s competitiveness with enough recommendations to preoccupy the EU agenda for years to come.

Indeed, I suspect that the Draghi report is far more likely to “reset” Britain’s relations with the EU than anything Starmer is likely to negotiate. Much of the commentary on the Draghi report has tended to focus on how difficult it will be to implement some of his more eye-catching proposals, particularly where they require unanimity of member states. I wrote about some of them here. But there is a huge amount in the report on how to deepen the single market that the Commission can deliver on its own and many of those have found their way into the mission letters handed to the new Commissioners. As I say in the TNE piece:

To the extent that the new Commission makes any progress on its economic agenda, it will be driven by the Draghi report. That report may make no mention of Britain yet nearly everything that it recommends - on industrial subsidies, reforming EU competition law, boosting research and development expenditure, deepening EU capital markets, integrating EU energy markets, promoting defence industry integration - will have huge implications for Britain.

Yet astonishingly, the British government appears to have made no attempt to engage with Draghi while he was writing his report. Nor can I find any analysis by a British think-tank or media outlet to try to analyse the implications of the report for Britain. This strikes me as extraordinary complacency by a British political class that in the eight years since the referendum seems to have ceased to pay attention to what is happening on the continent. Yet I predict that the government will spend the next five years trying to influence from the outside the way that the Draghi report is implemented. Of course, the easiest way would be to get back on the inside.

2. Real Conservatism

I hadn’t intended to write anything about the Conservative party conference which starts this week. In fact, I have tried to avoid mentioning the Tories in this newsletter since the election. Given the state in which they left the country, in common I am sure with most readers, my view has been that if we never hear from most of them again, it will be too soon. In any case, for the next five years, nothing they say or do is likely to be of any consequence for the political economy of Britain, Europe or the world, and so they are beyond the scope of Wealth of Nations.

Nonetheless, I changed my mind after reading this intriguing essay by Jesse Norman. Norman is one of the more thoughtful Conservative MPs, the author of excellent books on Edmund Burke and Adam Smith as well as a highly readable historical novel, and his reflections on the state of the party draw deeply on his historical and philosophical insights. But while his essay is on the surface a rather scholarly analysis of what constitutes the essence of real conservatism, it contains some fierce criticisms of how far his party deviated from this over the last 14 years.

The core of Norman’s analysis is that the Tories ceased to defend and uphold the British constitution and instead embraced alien, radical anti-democratic notions of the will of the people which led them to attack the very institutions that true conservatives should cherish and conserve. As Norman says:

One useful definition of a conservative is “someone who regards institutions as wiser than individuals”. Respecting the constitution means, among much else, setting one's face against referendums, supporting sensible reforms of Parliament, and seeking to slow down and discipline the vast flood of recent legislation by insisting on more notice and more scrutiny – and making a clear commitment to be bound by them as well.

Indeed, Norman is particularly scathing on referendums, of which the Tories held three in the last 14 years, on the Alternative Vote, on Scottish Independence and on Brexit, “all of which cast a complex issue or set of issues into a supposedly simple one-off choice in a yes/no format, and all of which proved to be intensely – and progressively more – divisive across both politics and wider society.”

Worse:

The stakes are raised when, as some Conservatives did during the process of Brexit, protestors or their political leaders claim that their position represents "the will of the people", or when they anoint themselves as “the voice of the people”. And they are raised again when sections of the media denounce their supposed opponents as “enemies of the people”, as the Daily Mail famously described three senior judges on its front page in November 2016.

Norman goes on to highlight numerous other ways in which the Conservatives conducted themselves in unconservative ways in office. They include the 2012 NHS reforms, first announced within two months of the 2010 election, and enacted with a minimum of prior consultation; the lack official consideration of the implications and impact of Brexit before the 2016 referendum was announced; or before the announcement of the 2050 Net Zero target, put through in a piece of secondary legislation; the Liz Truss “dash for growth” in 2022, which was assembled in less than three weeks, after the removal of the most senior Treasury official, and without external review and assessment; the huge increase in the turnover of ministers, especially after 2019; the downplaying of the role of Cabinet.

What is striking is that this sort of analysis has not formed any part of the argument in the Tory leadership election. Instead the four remaining candidates have settled into a comfortable narrative that what sunk the party was a lack of competence or unity or a failure to deliver on promises of low taxes or to cut immigration. That has led them down even less conservative blind alleys, threatening to withdraw for the European Court of Human Rights or attacking institutions such as the Treasury and Office for Budget Responsibility. There has been no hint of acknowledgment let alone apology for the party’s constitutional abasement.

The temptation for the Tories is to look at the current political difficulties faced by the Labour government and wait for the pendulum to swing back their way. But as Norman says, that is complacent: “it is quite possible that without drastic remedial action the Conservative parliamentary party will be wiped out altogether come the next election in 2028-9.” But until the Conservatives accept that it was their own lack of conservatism that led to their annihilation, there can surely be no redemption.

3. France vs Spain

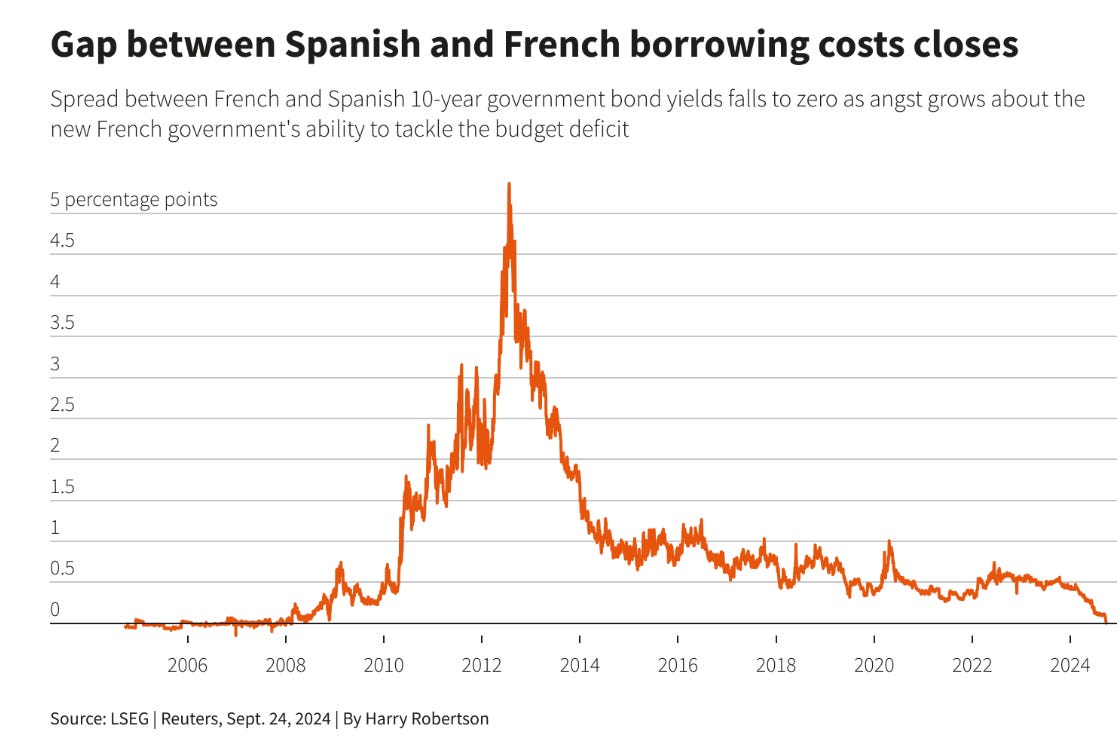

There was some excitement in the markets this week when French bond yields rose above Spanish bond yields for the first time since the global financial crisis. It was a symbolically significant moment. France has long been considered one of the “core” eurozone countries and thus one of the blocs safest sovereign credits, whereas Spain was famously one of the PIIGS (along with Portugal, Ireland, Italy and Greece) whose borrowing costs soared during the eurozone debt crisis, raising doubts about the future of the single currency. Now it is France whose political instability and fiscal challenges are the focus of investor concerns, whereas all the former PIIGS other than Italy can now borrow more cheaply than Paris.

Spain’s recognition from the markets has been a long time coming. Despite its own issues with political stability in recent years, it has for a long time now been one of Europe’s success stories. In the aftermath of the eurozone debt crisis, in Spain’s case fuelled by a property boom and bust, the then-Conservative government cleaned up the banking system and undertook a series of of structural reforms of labour and product markets that revived the country’s competitiveness. At the same time, Spain’s entrepreneurial businesses engineered an export boom that compensated for the sluggish domestic economy. Over the last decade, it has consistently been one of the fastest growing economies in the eurozone, admittedly a low bar.

Indeed, Spain is only likely to extend its competitive advantage in the coming years, in large part due to its remarkable success in the transition to renewables. Spain’s energy costs are already 60 per cent cheaper than those in Germany and, as this piece in the Wall Street Journal, wholesale electricity prices fell below zero for 12 per cent of all hours last year. That number is expected to rise sharply as more solar panels and turbines are installed. Indeed, Spain’s competitive advantage means that some French firms are already switching all the production that they can to Spain, while some analysts expect energy intensive industries to start relocating to Spain from northern Europe in the coming years to take advantage of cheaper energy.

As for France, the near-term outlook looks much less promising. After months of political turmoil, President Emmanuel Macron has finally appointed a prime minister, Michel Barnier, the veteran conservative politician and former Brexit negotiator. But the core challenge that triggered the turmoil remains: to pass a 2025 budget that will comply with eurozone fiscal rules by putting the deficit back on a path to hit 3 per cent by 2028, compared with an estimated 6 per cent this year. There is no guarantee that Barnier will be able to pull this off, or that even if he did, it would be enough to quell market doubts about France’s political and economic trajectory.

As Bank of America noted in a report this week, on economic fundamentals, France has a lot going for it:

On the economics side, we stand by our view that there is still a lot to like in French fundamentals versus European peers: better demographics, a more robust energy mix, less exposure to autos and/or Chinese end-demand and robust domestic demand.

But while the best bet is that Barnier is able to cobble together a budget that does the bare minimum to comply with eurozone fiscal rules, delivering some modest fiscal tightening this year, the likelihood that he is able to set out a credible plan to get borrowing back below 3 per cent of GDP by the end of 2028 looks remote. Meanwhile the markets will be on the look out for any attempt to unwind past reforms, not least Macron’s flagship pension reform, or to raise taxes as opposed to cut spending, thereby weakening the growth outlook. And even if a successful budget removes the risk of immediate budget collapse, the focus may then switch to possible snap elections next year, which can be held one year after the last ones in July.

4. China’s Draghi Moment?

Of course, France’s economic weakness will only add to fears of wider eurozone stagnation, adding to pressure on the European Central Bank to cut rates at its next meeting in October. But could some help be at hand, courtesy of the Chinese politburo? I wrote last week about the risks of Japanification of the Chinese economy as a result of Beijing’s failure to acknowledge the extent to which the country risks slipping into a balance sheet recession, i.e. a recession driven by a collapse in economic activity as firms and households unwind excessive debts.

This week, the Chinese authorities did finally act, announcing a package of measures that some likened to Mario Draghi’s “Whatever it takes” moment that saved the eurozone. First, the central bank announced sweeping interest rate cuts and other easing measures which it said would save 50m households about 150bn yuan ($21bn) a year in lower mortgage payments. Then the country's top leaders pledged to deploy "necessary fiscal spending" to meet this year's economic growth target of 5 per cent. According to Reuter, the government plans to issue special sovereign bonds worth about 2 trillion yuan ($284.4 billion), half of which will be used to stop local councils going bust and the rest to encourage spending by households and firms.

Perhaps most intriguingly, the central bank also announced an 800bn Yuan fund to boost the stock market, part of which will be used to help firms buy back their own shares. All this was enough to send the Chinese stock market soaring. The CSI 300 index of Shanghai- and Shenzhen-listed companies was up 15.7 per cent for the week in its best performance since November 2008, when China announced a similar stimulus package in response to the global financial crisis. Meanwhile Hong Kong’s Hang Seng index rose 3.6 per cent, up 13 per cent since the start of the week in its biggest weekly gain since October 1998 during the Asian financial crisis.

Will it be enough? As the Economist noted, the size of the stimulus package comfortably exceeded expectations. It also sent a powerful signal:

In a video conference on September 26th, the central bank’s leaders told branch officers to “go all out” in implementing the Politburo’s vision. Other officials may be getting a similar message. “As saving the economy and rescuing markets…become politically correct, we believe officials are likely to jump on the bandwagon to display their loyalty,” wrote Ting Lu of Nomura, a bank.

On the other hand, the stimulus amounts to 1.4 per cent of GDP, well short of the 4 trillion yuan stimulus that Beijing launched in 2009, equivalent to 12 per cent of GDP. Whether this will meaningfully life growth, ReutersBreakingviews has its doubts:

All in all, the 2 trillion yuan package reported by Reuters could increase GDP by 0.4% over the course of next year, reckons Capital Economics. Anything more substantial and long-lasting, though, will require not only more fiscal spending, but a redirection of the funds to tackle structural issues. Analysts at Morgan Stanley estimate it will take 10 trillion yuan, with most of the funds going toward pensions and healthcare, over the next two years to meaningfully lift growth.

Indeed, the bond markets suggest that Japanification fears have not gone away, with the yield on China’s 30-year government bonds on track to fall below its Japanese equivalent for the first time in about two decades. As Spain showed, the only sure way out of a balance sheet recession is determined action to recognise losses, recapitalise the banking system and remove impediments to the functioning of markets so that the economy can rebalance. Until it is clear that this is what Beijing really does intend, soaring Chinese stock markets are a good opportunity to sell.

5. Debt-for-Nature Swaps

I’ve written a few times about the growing African debt crisis which is not only a disaster for the countries concerned but has political, economic and social ramifications for the rest of the world, not least Europe. This piece in The Conversation sets out the scale of the problem:

The statistics are stark: 54 governments, of which 25 are African, are spending at least 10% of their revenues on servicing their debts. Among them, 23 African countries are spending more on debt service than on health or education.

As the authors say, the current crisis may not yet be a systemic threat to the global economy in the way that it was in the 1980s when multiple countries defaulted on their debt, it amounts to a “silent” sovereign debt crisis. The crisis compounded by the inadequacy of the current G20 Common Framework for dealing with the debts of low income countries, which is much too cumbersome. Zambia, for example, has been working through the G20’s cumbersome process for more than three and a half years and has not yet finalised agreements with all its creditors.

The authors are proposing an intriguing solution that could deliver substantial debt via a simplified process that should work to the advantage of all stakeholders:

First, the official creditors and the IMF should create and fund a strategic buyer “of last resort” who can purchase distressed (and expensive) debt at a discount from bondholders. The buyer, now the creditor of the country in distress, can repackage the debt and sell it to the debtor country on more manageable terms. The net result is that the bondholders receive cash for their bonds, while the debtor country benefits from substantial debt relief. In addition, the debtor and its remaining official creditors benefit from a simplified debt restructuring process.

There is a precedent for such buybacks. In 1989, the World Bank Group established a Debt Reduction Facility, which helped eligible governments repurchase their external commercial debts at deep discounts. It completed 25 transactions which helped erase approximately US$10.3 billion in debt principal and over US$3.5 billion in interest arrears. Some individual countries have also bought back their own debt. In 2009, Ecuador repurchased 93% of its defaulted debt at a deep discount. But as the authors say, most countries currently in debt distress lack sufficient foreign reserves to pursue such a strategy. Hence, they need to find a “friendly” buyer of last resort.

The key, of course, is persuading bondholders to take part. They are typically the biggest obstacle to debt restructurings, despite having been typically paid a premium to compensate them for the extra risk and thus received large returns on their bonds. By offering them cash for bonds that are already trading at a substantial discount, this may offer them a quick and attractive way out.

Meanwhile, on the subject of African debt, I was heartened by this piece from Reuters on another novel approach to providing relief. I had never heard of debt-for-nature swaps before, though it turns out there have been a number in recent years. Ecuador, Barbados, Belize, Gabon and Seychelles have all made such swaps in recent years, whereby bonds or loans are bought and replaced with cheaper debt, with savings used for environmental protection. Now Reuters reports that at least five African countries are working on what could be the world's first joint "debt-for-nature" swap to raise at least $2 billion to protect a coral-rich swathe of Indian Ocean.

The "Great Blue Wall" is a conservation plan that aims to protect and restore 2 million hectares of Indian ocean ecosystems by 2030, benefiting some 70 million people in coastal communities. It is an essential part of of a global target to protect protect 30% of the world's seas and land by the end of the decade, up from 1-2% now, under a landmark deal struck in 2022. But delivering on that plan requires getting more finance to developing countries, many of which are already on the frontline of the climate crisis. Debt-for-nature swaps sound like an excellent way to do it.

Really interesting re Jesse Norman whom I have met. Saying the unsayable is the only way forward for the moribund conservatives. Jonathan Sumption echoed the same sentiments about what a developed democracy actually is. We must have faith in our institutions and trust our politicians to make the best decisions on our behalf.