Bursting the AI Bubble

Bursting the AI Bubble

Things that have caught my eye this week, including America's imminent recession, tech's bad bets, Japan's latest experiment, Israel gone rogue, and why Trump could not have done the Gershkovich deal

1. The Sahm Rule

Is the American economy on the brink of recession? Bafflingly, just one week after the publication of data showing that the US economy grew by 2.8 per cent in the second quarter, fears of an imminent recession were enough to trigger a big market sell-off at the end of last week, with the yield on the 10-year US Treasury bond suffering its biggest weekly fall since the start of the year. Apparently it is all the fault of the Fed, which failed to cut interest rates on Wednesday, even though no one expected it to and the central bank hinted strongly that it would start doing so in September.

True, there is plenty of data to suggest that the US economy is starting to cool as a result of prolonged high interest rates, raising the prospect of what had begun to look like a perfect soft landing from high inflation into a hard landing. According to this piece by Paul Krugman in the New York Times, it all comes down to the jobs market and something called the Sahm rule.

The Sahm rule, named after former Fed economist Claudia Sahm, holds that a recession is probably underway if the average unemployment rate over the past three months has risen 0.5 percentage point from its most recent low. After Friday’s US employment data, which showed that just 114,000 new jobs were added in July, well below the 175,000 that were expected, this threshold has now been passed. That has sparked fears among investors that the economy may be cooling even more quickly than expected, and that a big rate cut will now be needed in September, or even earlier, to forestall a deeper recession, hence the fall in Treasury yields.

As Krugman points out, there were lots of predictions of imminent recession in 2022 based on a single indicator, in that case an inverted yield curve. Those didn’t come true, and he thinks these latest predictions won’t come true either. He puts the rise in unemployment down to a surge in new entrants to the workforce, in part due to immigration but also those with disabilities seeking work, and the time it takes for them to find jobs. So his conclusion to the triggering of the Sahm rule?

Don’t panic; it probably doesn’t mean that we’re in a recession. But the Fed should definitely be cutting rates.

2. Artificial Valuations

On the other hand, could the market sell-off last week be the first signs of the bursting of a stock market bubble? Barely two weeks ago, the S&P500 index of leading US shares hit an all-time high valuation of $47 trillion. But as this piece in Intelligencer notes, on that day just seven companies accounted for a third of that valuation, amid expectations that AI was going to lead to a productivity revolution. Since then, shares in Microsoft, Apple, Amazon, Nvidia, Meta, Alphabet and Tesla have tumbled as investors question the vast sums being invested in AI. In their latest quarterly reports, the big tech companies reported a 50 per cent rise in spending to over $100 billion this year, with some analysts predicting spending of $1 trillion over the next five years. Meanwhile Intel, which manufactures computer chips, fell 26 per cent on Friday alone. The tech heavy Nasdaq index is now in official “correction” territory, having fallen more than 10 per cent from its July peak.

I have a confession to make. I’ve found all the hype around AI over the last few years a giant yawnathon. I’m not a Luddite. I’m excited about the power of technology to revolutionise our lives with advances in clean energy, personalised medicine and precision fermentation which has the potential to transform food systems. But I’ve not been able to see much point of these chatbots other than as a way for students to cheat on essays. At best, AI seems to be a brand being attached to any new digital application, some of which may be useful. At worst, it seems like a very expensive solution looking for a problem. A few weeks ago I moderated a panel of tech executives and was still none the wiser. I’m not sure the audience were either.

But now it seems my scepticism may have been warranted. As the Intelligence piece notes, there has recently been something of an investor vibe shift:

It is commonplace now to denigrate something mediocre or sloppy as having been created by AI. Earlier this year, Goldman Sachs issued a deeply skeptical report on the industry, calling it too expensive, too clunky, and just simply not as useful as it has been chalked up to be. “There’s not a single thing that this is being used for that’s cost-effective at this point,” Jim Covello, an influential Goldman analyst, said on a company podcast.

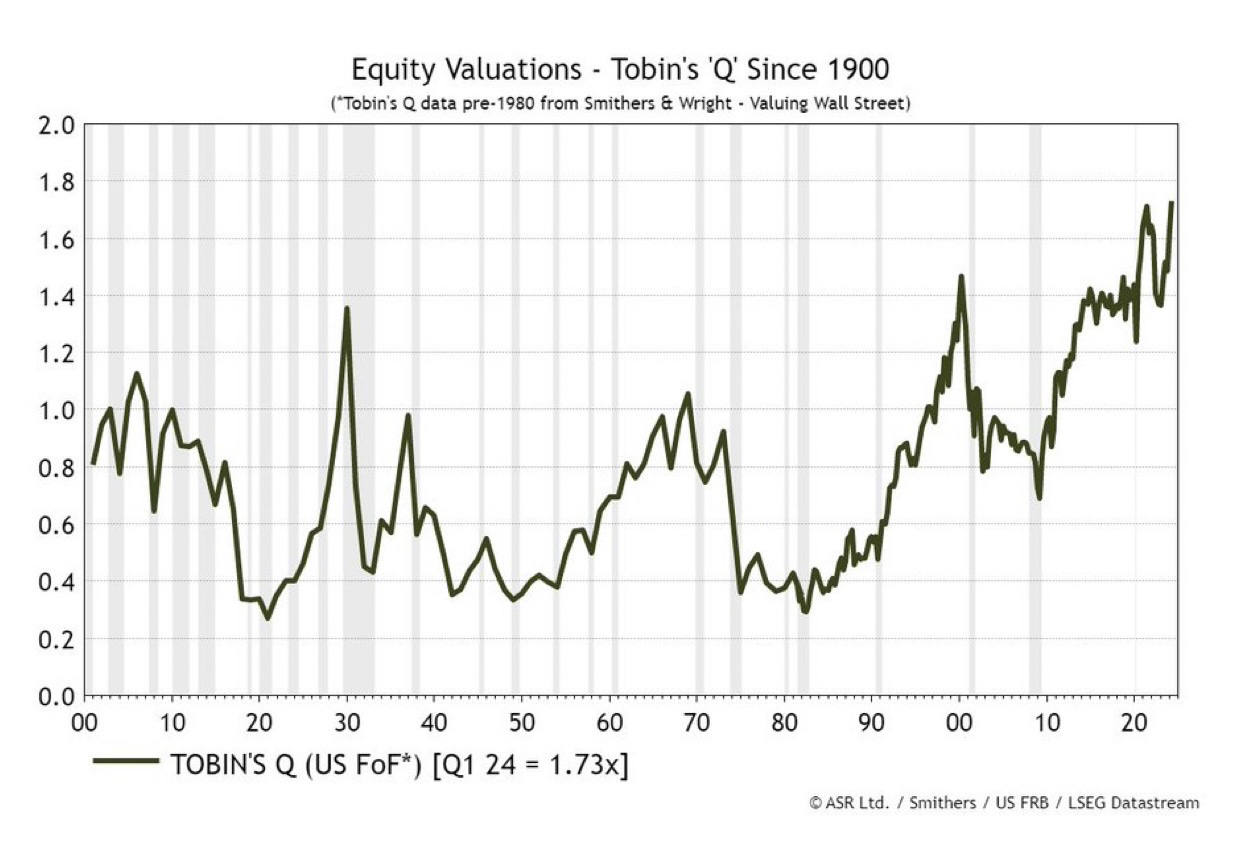

The bullish view is that this is just the froth coming off the top of a heady market, and that investors have simply been rotating into less glamorous but undervalued sectors. As the Intelligencer piece notes, the Russel 2000 index of smaller stocks has risen 11 per cent since the tech rout. But I keep returning to this chart published by Ian Harnett of Absolute Strategy Research just before the rout started which looks at Tobin’s Q, the ratio between a physical asset's market value and its replacement value. One used to hear a lot about Tobin’s Q during the height of the dotcom bubble. As Harnett says, there is a debate about its theoretical basis and empirical calculation. But it is hard not to look at this chart and think: bubble.

3. Japanese Experiments

As if investors didn’t have enough to worry about, the steepest stock market falls this week were not in America but in Japan, where the Nikkei 225 index fell by nearly 6 per cent in a day. That was its biggest one day decline since the pandemic and a clear signal of dark clouds looming in the land of the rising sun. The Japanese stock market has had a strong run, up by about a third in the year to July. That was fuelled in part by the decline in the value of the Yen which three weeks ago was trading at a 38 year low, reflecting the difference in interest rates between Japan, where they remained close to zero, and other major economies, where they had risen to combat inflation.

But last week, as other central banks were debating whether to cut interest rates, the Bank of Japan surprised the markets by not only raising them but scaling back its purchases of government bonds under its quantitative easing programme. Its problem is that the weak Yen is starting to raise domestic inflation pressures, while earlier attempts to intervene in foreign exchange markets to boost the currency had failed. The result is that the Yen is now up eight per cent in three weeks. But as the WSJ notes in this editorial, there are risks in this reversal of a decades-long policy of ultra-cheap money that has persisted since the Japanese property market collapsed in 1992:

One reason to move slowly in tapering Japan’s quantitative easing is that other buyers will have to be found for Japanese government bonds, of which the BOJ currently holds about half the outstanding issuance. Tokyo reportedly is lining up brokers to market more of the bonds to global investors.

One unknown is whether or how such capital inflows—coupled with a slowing or reversal of Japan’s famous outbound carry trade as domestic rates rise—will affect the yen or other financial markets such as the U.S. Another unknown is how a Japanese economy marked by zombie companies and other legacies of ultracheap money will adapt to slightly higher rates.

As the WSJ says, “Japan continues to be the world’s biggest monetary experiment, and the most perilous”. The markets are right to be nervous.

4. Gone Rogue

Although it is always hard to discern the extent to which geopolitical risks are driving markets, it would be surprising if these were not playing on investor nerves too. Israel’s assassination of last week of Fuad Shukr, the right-hand man of Hezbollah leader Hassan Nasrullah, with a drone strike in Beirut, and then Ismael Haniyeh, the long-time political chief of Hamas, in central Tehran marks an alarming escalation in Middle East tensions. The fact that Benjamin Netanyahu is prepared to assassinate Hamas’s lead negotiator would appear to suggest that he has no interest in a ceasefire and hostage deal but raises the spectre that he is trying to draw America into a war with Iran. It was also timed just days after a new Iranian president took office seeking closer relations with the West. As Michael Burleigh notes in this piece for the i:

We have therefore reached the point of maximum danger, as is indicated by upward movements to the price of oil. Iran will be weighing up whether to strike back directly again, or to act through its proxies. The US will urge restraint… even as it supplies Israel with plane-loads of sophisticated munitions.

As Burleigh says, there is a way out of this crisis. Netanyahu could declare “mission accomplished” and greenlight the ceasefire and hostage deal, which could offer Hezbollah, the Houthis and even Tehran a way out of the conflict. Given that the Knesset is on summer recess, he doesn’t risk the immediate collapse of his coalition. But nothing in Netanyahu’s behaviour suggests that he is likely to take this path. Joe Biden is sending more warships to the Mediterranean and has recommitted to guarantee Israel’s security. Indeed, as this report from Axios indicates, America seems to have lost all control over its ally, which appears to have gone rogue. Ominous.

5. Freed Evan Gershkovich

The release of Evan Gershkovich alongside other Western hostages in a prisoner swap with Russia is wonderful news. The wrongful imprisonment of the Wall Street Journal reporter on trumped up charges of espionage was an outrageous assault not just on a young man doing his job, but on journalism itself. Even if the nature of the prisoner swap, which involved the release from German captivity of a convicted murderer, raises some difficult ethical questions, there is no question that the exchange was a remarkable piece of diplomatic deal-making by the Biden administration, as is clear from this extraordinary forensic account by the Wall Street Journal.

It is testimony to Joe Biden’s decades of commitment to alliances and the trust that he has built with allies that he was able to do this deal. Donald Trump used to claim that only he could get the hostages back, and now suggests that Biden may not have struck a hard enough bargain. But the reality, as this thread on X by Christo Grozev, an associate of Alexey Navalny who was originally supposed to be part of this deal before he was murdered, makes clear is that Vladimir Putin almost certainly did the deal now with Biden because he knew Trump could never have pulled it off.

This is an excellent analysis of current geopolitical issues.

WRT the broader impact of AI, where I think we'll see the first substantial impact on the job market will be in the low/mid-range SMEs (subject matter experts). Their skill set, resembling conceptually an AI-generated level of polish, is immediately vulnerable and will be under pressure fairly soon.

This would include those currently in customer support, technical writers, etc.

Jobs that require human nuanced responses--that metaphysical element exemplified by such intangibles as "bedside manner", and to a degree, high-end sales, will persist longer.

Just guesses, though.

Sometimes I wonder if the homeless situation that we see in large urban areas in many industrialized democratic or republican nations is not the first edge of this trend, preceding the advent of AI, but a symptom of the same pressures that AI will leverage. By this I mean that while the modern homeless situation is a complex ball of yarn, so far as causes, I postulate that a large section of it is simply people who have insufficient skills to meet any current market demand for employment; they are not drunks, they are not addicts, they simply possess general skills that in former times could have earned them a living, but are insufficient today. This is to say, bluntly, that they have no contributory value to society in an economic sense, nor will they in any foreseeable system.

There has always been an element of this is the modern American workforce, but I perceive that this is a very much larger problem at this time, and it's growing: unemployability of significant numbers of essentially average humans.