Civilisational Erasure

Thoughts on Trump's very bad options, the birth of the Petroyuan, the Trump Syndicate's lucky bets, tough times for Europe's MAGA right, and a film to help understand why we are where we are

Here’s this week’s newsletter. By popular demand, I’ve stuck to my usual formula of writing too much. Many thanks to those who took the trouble to provide feedback to say that they preferred it this way. Of course, it takes a lot of work, so if you think that it was worthwhile please consider showing your appreciation by becoming a paid subscriber. Other ways to show your support include sending it to your friends and family, hitting the like button and leaving a comment. Have a good week!

In today’s newsletter:

Trump’s Bad Options: Pressure Index

Birth of the Petroyuan? Squandering exorbitant privilege

The Trump Syndicate: Prophets of Greed

Europe’s MAGA Right: Civilisational erasure

Palestine 36: Where it began

1. Trump’s Bad Options

It shouldn’t have come as much of a surprise, at least to Wealth of Nations readers, that Donald Trump TACOed last week. Not only would carrying out his threat to obliterate Iran’s civilian energy infrastructure have constituted a grotesque war crime, it would have risked near-certain retaliation against the critical infrastructure of the entire Gulf region and likely led to a global financial crisis. As noted last week (see TACO time):

The lesson of last year is that faced by an adversary with escalation dominance, Trump does indeed Always Chicken Out (TACO). The relatively muted market reaction to the war so far (see Will Iran Trigger a Financial Crisis?) suggests that this is what investors expect will happen this time.

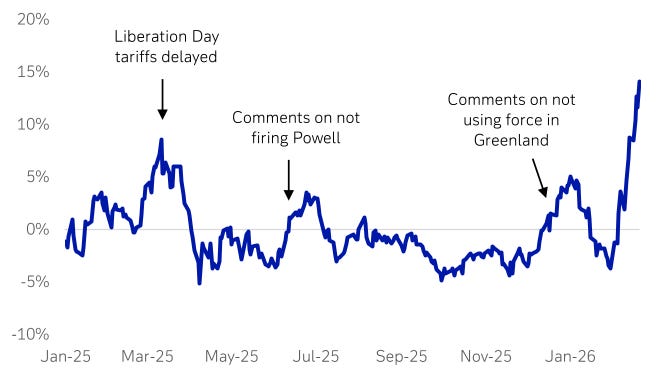

As it happens, Deutsche Bank has constructed a useful cart of what it calls the “Pressure Index” which captures Trump’s propensity to fold in the face of resistance to his frequent brinkmanship. It uses an equal weight index of the 1 month change rate in approval ratings, 1 year inflation expectations, S&P 500 performance and US treasury yields. Here is where it stood on the eve of last week’s TACO. The index will only have soared since then.

That said, the sharp sell-off in bond and equity markets on Friday was a sign of market nervousness that the predictive power of the Pressure Index may have broken down over Iran. It is abundantly clear that the Trump administration has lost control of the situation, the outcome no longer entirely in its hands.

It has only deferred its threat to obliterate Iran’s energy infrastructure until April 6. That is ostensibly to buy time for the US and Iran to reach a negotiated settlement. Trump insists that the Iranians are desperate for a deal, that his administration is talking to the “top people” and that they gave him a “present” as a gesture of goodwill. The Iranians say that this is nonsense and that America is negotiating with itself. It has come to something when one is more inclined to take the word of the Islamic Republic over the President of the United States. It was striking that there were no US or Iranian representatives at a meeting of regional foreign ministers in Pakistan this weekend to discuss the crisis.

One must, of course, be open to the possibility that Trump will be vindicated and will achieve through diplomacy his objectives as set out in a 15-point plan presented to Iran last week. They included demands that Iran dismantle its nuclear capabilities, curb its missile programme, abandon support for regional proxies and reopen the Strait of Hormuz. But it is hard to find anyone with serious diplomatic expertise who thinks that is likely. Instead, Tehran has responded with its own maximalist demands, including recognition of its control over Hormuz and its right to charge a fee to all ships passing through it.

That leaves Trump with two options, neither of of them good:

Declare victory and go home, though this would leave the Iranian regime in place, still in control of Hormuz and in possession of its nuclear stockpile so would in the eyes of the world be a humiliating defeat for America

Escalate by using the 17,000 troops mustering in the Gulf to launch a ground offensive with an objective to occupy some islands to put pressure on the regime, or take control of the Strait, or seize the nuclear stockpiles

Trying to guess what Trump will do next is a mug’s game. Nonetheless, it is hard to believe that having dispatched so many troops to the region, with another 10,000 potentially on their way, he won’t try to use them. Indeed, over the weekend he appeared to signal as much with a Truth Social post encouraging his followers to watch a Fox News segment in which veteran analyst Mark Levin advocated a limited ground operation to recover the nuclear material. If successful, this would at least allow Trump to claim to have achieved one of his war objectives. But it comes with two huge risks.

The first is that an operation to recover the nuclear material will be far from straightforward. According to the WSJ, the assumption is that around half of the enriched uranium is stored in underground tunnels near Isfahan with the rest in a cache at Nantaz - and that trying to grab it would require “potentially the largest special forces operation in history”:

Army Rangers or other combat troops would be needed to secure perimeters, former military officials said. Engineers with excavating equipment would be needed to dig through the tons of debris blocking entrances to Iran’s subterranean nuclear complexes and check for mines and booby traps.

If a local airfield wasn’t available, a makeshift one would need to be set up to fly equipment in and the material out. And ground forces and aircraft would need to be prepared to head off Iranian drone and missile attacks. A quick response force would need to be on hand in case more troops had to rush to the scene, former military officials said.

Of course, the potential for such an operation to go wrong, even if specialist forces have trained for it, is immense. But the second problem with this exit strategy is that it will leave Iran in control of Hormuz, still able to charge its tolls. Marco Rubio, the US Secretary of State, pretty much conceded last week that the US was likely to leave the Hormuz toll problem unresolved for others to sort out:

‘Not only is this illegal, it’s unacceptable, it’s dangerous to the world, and it’s important that the world have a plan to confront it.’

‘What we’ve said is that the countries that are most impacted by that (should) be willing to do something about it, and we’ll help them. We’re willing to be a part of that coalition, but we’ve encouraged others to sort of put it together.’

Leaving aside the hypocrisy of the Trump administration’s late discovery of the merits of international law, it seems pretty clear that this war - and the consequent disruption to oil, gas, fertiliser and helium supplies with all the knock-on effects for the global economy - has some way further to run. Expect the Pressure Index to continue to run higher - and markets to have further to fall.

2. Birth of the Petroyuan?

Could one casualty of a prolonged Iran war be the use of the US dollar in global trade and savings and its role as the world’s reserve currency? So far, the dollar has benefitted from some degree of safe haven flows since the start of the conflict, but these have been puny compared to past shocks.

One reason is that interest rate differentials are not moving in the dollar’s favour, reckons George Saravelos, Deutsche Bank’s chief currency strategist. Other central banks have been much more hawkish this time than during the energy shock of 2022. The Bank of England, Bank of Japan, Riksbank, and ECB have all expressed a willingness to raise interest rates to head off inflation risks. The market now expects two interest rate hikes this year by the ECB and BOE.

At the same time, there are signs that Asian and Middle Eastern central banks will respond to higher import bills by running down FX reserves and excess savings rather than borrowing. This has the twin advantage of preventing their currencies from weakening so lessening the inflation shock, while preserving domestic fiscal space. But the corollary is that it also reduces US fiscal space by putting upward pressure on US Treasury yields. That is not dollar bullish.

Meanwhile, Deutsche Bank points to another long-term risk to the US dollar: the possible impact on the petrodollar regime:

The world saves in dollars in large part because it pays in dollars. The dollar’s dominance in cross-border trade is arguably built on the petrodollar: globally traded oil is priced and invoiced in USD. This arrangement can be traced to a deal struck in 1974 where Saudi Arabia agreed to price oil in USD and invest surpluses in USD assets, in exchange for US security guarantees. Because oil is a core input to global manufacturing and transport, there is a natural incentive for global value chains to dollarize, and global surpluses to accumulate in USD.

The foundations of the petrodollar regime have been under pressure even before this conflict. Most Middle East oil is now sold to Asia not the US; sanctioned oil from Russia and Iran has already been trading off dollar rails; Saudi Arabia has been localizing defence, and experimenting with forms of non-dollar payment infrastructure such as Project mBridge.

The Iran War could deepen these fault lines, not least by challenging the US security umbrella for Gulf infrastructure and the maritime security for global trade in oil. Not only did the Gulf states have around $2 trillion of investments planned in the US that must now be in doubt, but damage to Gulf economies could encourage an unwind in their foreign asset savings.

What’s more, if Iran succeeds in imposing a toll payable in Yuan for the passage of ships through Hormuz, that would have a further impact on the dollar. After all, many Gulf States may conclude, however reluctantly, that in the medium-term at least, it is better to pay these tolls than risk their own ground offensive:

The conflict could be remembered as a key catalyst for erosion in petrodollar dominance, and the beginnings of the petroyuan.

Even longer-term, Deutsche Bank notes, the risk is that the Iran War leads the world to accelerate their move away from globally traded oil and gas towards more resilient sources of energy including domestically available fuels, renewable energy, and nuclear power.

The energy choices of the Global South, Europe and North Asia will be key to track. A move away from oil could be as powerful as the pressure to price it in other currencies.

Perhaps Donald Trump’s most legacy-defining contribution to US history will have been the president that squandered America’s exorbitant privilege.

3. The Trump Syndicate

Perhaps the most shocking story - though as always with anything Trump-related, not necessarily the most surprising - was the half a billion dollar’s worth of bets placed in the oil markets minutes before Trump published his Truth Social post announcing his Iran TACO. That inevitably raised suspicions that someone close to Trump may have been profiting from inside information. As the FT reported:

The well-timed trades echoed the flurry of large highly profitable bets made on prediction market Polymarket on the timing of the US’s attacks in recent months on Iran and Venezuela.

“It’s hard to prove causality . . . but you have to wonder who would have been relatively aggressive at selling futures at that point, 15 minutes before Trump’s post,” said a market strategist at a US broker, referring to Monday’s trades.

Nor was that the only concerning story relating to the Trump family’s financial dealings to surface during the last week. Almost as shocking was the abrupt resignation of Margaret Ryan, the Securities and Exchange Commission’s enforcement chief, after just six months in the job, after reportedly being blocked by agency leaders from launching investigations into Trump family dealings.

Also last week, Republicans on a House Natural Resources subcommittee blocked a Democratic motion to subpoena Donald Trump Jr. to testify over his backing of critical mineral company, Vulcan Elements, that received a $620 million federal loan from the Department of Defense last year shortly after the president’s eldest son made his investment.

Of course, none of this adds up to evidence of wrong-doing. White House spokesperson Kush Desai told the FT:

The only focus of President Trump and Trump administration officials is doing what’s best for the American people… The White House does not tolerate any administration official illegally profiteering off of insider knowledge, and any implication that officials are engaged in such activity without evidence is baseless and irresponsible reporting.”

Nonetheless, I wrote last year about the growing concern in the markets at the Trump administration’s apparent merging of private and public interests. The Trump family is estimated to have increased its net worth by an estimated $4 billion since last year’s election (see Government for Sale). Some scholars have talked of Trump’s neo-royalist approach to international relations. Sir Paul Tucker, the former deputy governor of the Bank of England and now a fellow at the Harvard, Kennedy School, has coined the term “The Trump Syndicate”, which I think rather better captures the informal network inside and outside government that appears to be profiting directly from Trump’s decisions.

It goes without saying that any impression that US codes of conduct designed to maintain the integrity of public markets are not being properly enforced, or that access to government contracts and funds was dependent on political patronage, would be deeply corrosive to trust in US financial assets - and another reason to be bearish about the long-term prospects for the dollar.

4. Europe’s MAGA Right

I’m always being challenged by readers to write about more good news, so here is some. One of the happier outcomes of Trump’s Iran debacle is that it appears to have dealt a serious blow to many of the administration’s “civilisational allies” on Europe’s far right. In the last week alone, MAGA-aligned parties across Europe have suffered a series of setbacks:

In France, the far right failed to take key cities in last week’s municipal elections, blunting the sense of inevitability that Marine Le Pen — or her dauphin, Jordan Bardella, if she’s barred from running — would finally claim the presidency in 2027. In its prime southern targets of Marseille, Toulon and Nîmes, left-leaning and more moderate right-leaning voters teamed up in a so-called “Republican front” to keep it out.

In Denmark, Mette Frederiksen will remain as prime minister after her Social Democrats emerged from last week’s elections as by far the largest party, boosted by her tough stance opposing Trump over Greenland. The far-right Danish People’s Party improved its position in parliamentary elections but still fell well short of its pre-2019 support levels

In Hungary, a rattled Viktor Orban, now trailing by nine percentage points in the polls ahead of the April 14 general election, is resorting to shouting at voters in increasingly unhinged rants about Brussels and Ukraine. He has also set the police onto a well-known investigative journalist who exposed his corruption, citing trumped-up spying charges

In Slovenia, a far-right insurgency was shut out of power

In Germany, the AFD distancing itself from Trump amid evidence that the US president is deeply unpopular among voters. According to one recent poll, only 15 percent of Germans view the U.S. as a trustworthy partner

In Italy, Giorgia Meloni suffered a defeat in a referendum she had called on a judicial overhaul that few Italians understood which turned into plebiscite on her government. That has emboldened the opposition ahead of parliamentary elections next year

In Britain, Nigel Farage is losing his polling gloss, notes Bloomberg

All of that said, the good news ends there. Clearly, the Iran war has led to a deepening of the transatlantic rift, with growing fears that Trump may abandon Ukraine and NATO. President Zelensky has said that the Trump is making its security guarantees conditional on Kyiv agreeing to give up land in Donbass.

What’s more, the longer the Iran War continues, the greater the benefit to Russia via higher oil prices and the depletion of Western stocks of weapons. This week it was reported that the Pentagon was diverting funds from European governments to buy weapons for Ukraine to fund its own rearmament.

The reality is that the moment may be fast approaching when Europeans, their economies seriously weakened by the Iran energy shock, will be obliged to step up their support for Ukraine to prevent Kyiv being forced into a disastrous surrender. As I noted in my latest column for Kathimerini (not yet online):

Putin believes he is winning and, with Trump apparently on his side, sees no reason to back down. Only Europeans can change his calculus. That requires…Europeans to demonstrate that they truly regard this war as existential — and that they are prepared to make the necessary sacrifices, both economic and military, to win it.

5. Palestine 36

I don’t think I’ve offered a film recommendation here before, but having stumbled across Palestine 36 on Amazon Prime last night, I urge you to watch it too. It’s a historical drama set during the Palestinian Revolt of 1936-1939 that led to Britain’s Peel Commission becoming the first to formally recommend a two-state solution to the Arab-Jewish conflict. It is a period of history that is vital to understanding much of what is going on in the Middle East today, but which is also, as The Guardian reviewer noted, not taught in British schools. The film, which was the Palestinian entry to this year’s Oscars, was released in Britain last year and opened in many cinemas across America last week.

Inevitably, as with all historical dramas, it has prompted criticism over its factual accuracy - although the biggest gripes by this reviewer seemed to concern the uniforms and hairstyles of British military officers. But I thought it was pretty even-handed. Although the story is clearly told from a Palestinian perspective, and primarily focuses on the relationship between the British and Palestinians, it does not shy away from the conflicts among Palestinians themselves, nor the fact that many of those evicted from their lands either had no formal title to it, or had lost the right to farm it after it was sold to jewish settlers by absentee landlords.

Besides, it’s not the job of a historical drama to provide definitive histories. It has done its job if it shines a light on past injustices and encourages the viewer to delve deeper into a subject. There’s no question that, for a Brit, the film makes uncomfortable viewing, which may help explain why, shamefully, most British newspapers, other than The Guardian and Financial Times, neglected to review it. But at a time when, under the cover of the Iran War, Israel appears to have stepped up its ethnic cleansing of Gaza, the West Bank and southern Lebanon, the need to understand this chapter of history is more urgent than ever.

My comment elsewhere was that at least Zelensky may find there are benefits through deals with Gulf States.

It may be too much to hope that Epic Fury might lead to regime change in the US