Is France becoming the new Italy?

Is France becoming the new Italy?

French political instability poses risks to eurozone financial stability given its high levels of debt, while casting fresh doubts on the EU's ability to respond to existential challenges

It is a long-established principle of European Parliament elections that they have very little bearing on the workings of the European Union, but can have outsize effects on national politics. That was certainly true of the latest European Parliament elections whose votes were counted on Sunday. For all the talk of a “far right surge”, right-wing populist parties increased their vote share from around 20 per cent to 25 per cent. Even this may overstate the rise, given that Georgia Meloni has shifted her Brothers of Italy party towards the mainstream. The reality is that the centre held, with mainstream parties securing just over 450 of the 720 seats. That should be enough to secure Ursula von der Leyen a second term as Commission president.

Nonetheless, the elections still produced a political earthquake in the form of President Macron’s decision to dissolve parliament and call a snap general election after his Renaissance party was trounced in the polls, coming a distant second to Marine Le Pen’s National Rally. That did not just spook the European political class, but spooked the markets too with the euro and French and eurozone stocks falling sharply. The fear is that Macron’s gambit has opened the door to at best a prolonged period of political instability, and at worst, a eurosceptic, pro-Russian populist government. Is France becoming the new Italy, for so long the primary source of European instability? And if so, what this might mean for Europe more widely?

Italian Jobs

Indeed, French politics has been exhibiting Italian levels of instability for some time, albeit this is obscured by the presence under the French constitution of a strong presidency, just as Italian politics has recently been showing signs of becoming more stable. France has now had four prime ministers in four years and may in a few weeks time get its fifth, while Italy has had a mere three prime ministers since 2018 and Meloni looks safe in her job until the next election which doesn’t have to be called until the end of 2027. Similarly, just as Italy’s decades of political instability followed the destruction of the old party system following the Tangentopoli corruption scandal in 1992, so too current French instability reflects the hollowing out of the mainstream political parties following Macron’s own insurgency in 2018.

Of course, Macron’s gamble is that he can bring an end to this instability by forcing French voters to confront the reality of a far right government. In truth, his decision to call an election should not have come as such a surprise. A political confrontation with the National Rally was looking inevitable at some point this year. Macron’s Renaissance party lacks a majority in the National Assembly, leading to political paralysis. The president has already been forced to use his decree powers 23 times to secure his agenda, which has only further undermined his popularity and fuelled support for populist parties. A showdown over the budget later this year loomed, raising the prospect of the government losing its vote of no confidence.

Could Macron’s gamble pay off? National Rally only got 33 per cent of the vote. Add in support for smaller far right parties, and that rises to 38 per cent. But in France’s two round voting system, National Rally has traditionally struggled to increase its vote share when it becomes a two-horse race. The problem is that in France’s highly fragmented political system, there is no one party that looks likely to emerge as the main challenger to Le Pen. The risk is that even if Le Pen fails to secure a majority, which seems unlikely, nor will anyone else. What will emerge is an even more fragmented National Assembly, in which the mainstream parties struggle to put together a coalition, leading to further political instability and disillusionment.

Fiscal Fundamentals

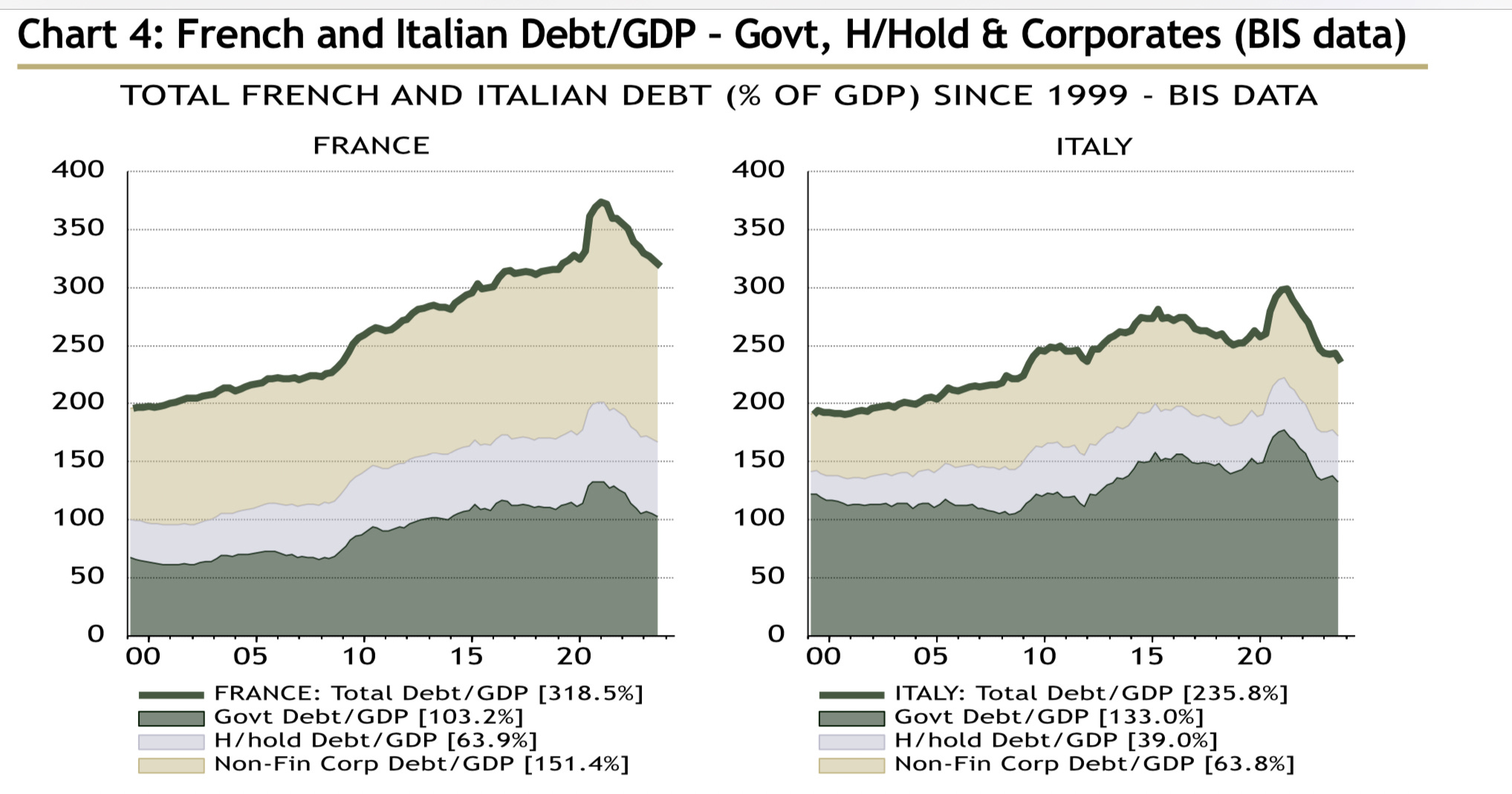

What makes this so worrying is that the parallels with Italy go beyond political instability. Another thing both countries have in common is very high debt loads and weak public finances. Days before the election Standard & Poors downgraded French government debt to AA- citing concerns that the government will struggle to meet its budget targets. Paris has already acknowledged that it will need to make an additional €20 billion of spending cuts to hit this year’s target of a deficit of 5.1 per cent of GDP. S&P reckons the government’s target of reducing the deficit to 3 per cent by 2027 looks out of reach. This comes as the European Central Bank in its latest Financial Stability Report flagged growing eurozone fiscal risks, warning that “fiscal fundamentals remain vulnerable to negative growth surprises and fiscal slippage”.

In fact, France’s debt problems are arguably worse than those of Italy. When one includes household and corporate debt, France’s debt burden is significantly higher than that of Italy. And as Ian Harnett at Absolute Strategy Research has noted, it is private sector debt, not public sector debt, that tends to be the key indicator for financial stress. Until now, there has been little sign that the market has been paying attention to France’s debt challenges. The spread of French government bonds over German bunds was less that 50 basis points, well below that of Italian bonds, while the cost of insuring French debt against the risk of default was well below that of the US, even though they have similar debt-to-GDP ratios. The slide this week in French government bonds and French bank stocks suggests this may be changing. French political instability risks leading to financial instability for France and the eurozone.

The broader question is whether French political instability will become a wider problem for the political functioning of the EU. The word existential gets bandied around too often in respect to crises, including by me, but the reality is that the EU - and Europe - is currently facing a series of challenges both external and internal that will determine for decades to come whether the continent is capable of being the architect of its fate, able to defend its interests at home and project them abroad, or will become like a latter day Holy Roman Empire, an ineffectual lose confederation of small squabbling states permanently at risk from more powerful external actors.

Holy Roman Empire?

The external challenges start with the need to strengthen Europe’s defences in response to Russian aggression, including how to enhance it military capabilities, boost military production and improve defence procurement. A related challenge concerns the vexed question of enlargement, given new urgency by the situation in Ukraine, but also relating to other neighbourhood counties such as the western Balkans and Georgia. There is also the question of how to respond to growing Chinese assertiveness. Then there are the long-standing questions of migration and control of the borders which the EU has been struggling to tackle for a decade, and the global challenge of climate change, while are at the top of the EU’s priority list.

Then there are the internal challenges, primarily relating to the functioning of the single market. As previously noted in Wealth of Nations, given that foreign policy begins at home, reviving the EU’s lacklustre growth is an urgent security challenge in its own right. The single market remains deeply dysfunctional in key industries crucial to Europe’s prospects, including energy, digital services, financial services and defence. After more than a decade of argument, the EU still does not have a complete banking union or functioning capital markets union, depriving the continent of capital. Energy markets remain deeply fragmented, as do digital services. The EU has 102 mobile telecom operators, compared to just three in America.

Finding common solutions to these common challenges will require further integration in areas that impinge directly on sensitive areas of national sovereignty such as foreign policy, judicial policy or energy policy. What’s more, no EU response to many of these challenges is likely to be effective unless underpinned by common funds. Yet the question of expanding the EU budget remains deeply divisive, pitching net payers against net recipients. Similarly, any attempt to reallocate funds from agriculture and regional support towards new strategic priorities such as defence or enlargement, provokes fierce resistance. Richer northern EU member states in particular remain fiercely opposed to common borrowing.

Finding solutions to these challenges may be hard but should not be impossible, despite the swing to the populist right in the elections. One only needs to consider what the EU has achieved in the five years since the last European elections: as Matina Stevis has noted in the New York Times: “the bloc jointly bought Covid-19 vaccines and started a massive economic stimulus programme to recover from the pandemic. It sanctioned Russia and paid to arm and reconstruct Ukraine. It ditched Russian energy imports and negotiated new sources of natural gas. It overhauled its migration system. It adopted ambitious climate policies”.

But Europe’s response to crises has traditionally been driven by Franco-German leadership. If France is about to succumb to greater political instability, where will the leadership come from now? Part of the answer may be Italy. There is no doubt that Meloni, who has good relations across the political spectrum, is emerging as a key player, praised by Thanasis Bakolas, the secretary general of the EPP this week for her “constructive approach” to EU problem-solving. Meanwhile one of her predecessors as Italian prime minister, Mario Draghi, has been mooted as a potential candidate for the powerful role of President of the European Council. As France becomes the new Italy, could Europe’s future hinge on Italy becoming the new France?

An excellent piece Simon. Thank you. The only observation I would make is that when it came to the euro area crisis of a few years ago, Greece was clearly fundamentally an issue surrounding government debt sustainability, made worse by money leaving the country (this could be tracked in almost real time, as the Central Bank published its balance sheet on a monthly basis); Spain more an issue of the substantial imbalances that were allowed to build up prior to the GFC (with the corporate sector running at the peak, a deficit of over 15% of GDP).

With Spain, the level of debt, private, or public, was less of the problem. With the GFC, inflows required to finance this deficit ceased, pushing the Spanish economy into a deep recession - just before Mario Draghi stepped with his promise to do whatever it takes, Spanish government bond yields seemed to danger of going through 7%, the trigger for Greece, Ireland and Portugal to all be pushed into the "bailout." What was also surprising at the time was that so many commentators expected Spain to bounce back relatively quickly.

As my colleague Marchel has also highlighted, recent months have also seen French banks significantly increase their exposure to non-domestic debt, a potential issue if interest rates stay high, for longer.

I will do more work on this in the next few days. Italy for sure has always had different economic fundamentals to France! Kind regards, David