Rupture? What Rupture?

Thoughts on Trump's economic victory lap, Kevin Warsh's fairy tales, America's embrace of neo-royalism, how to invest for regime change, and why Chinese tech is winning

Here is this week’s newsletter. A warm welcome to new subscribers. Thanks as always to the generous paid subscribers whose support makes this worthwhile. If you have been enjoying these posts this year, please do consider becoming a paid subscriber too. At the very least, please do forward it to anyone you think might be interested. I look forward as always to your comments and feedback. And please do email me if you have questions or ideas for future posts.

Trump’s Victory Lap: Rupture? What Rupture?

Game of Chairs: Warsh’s Fairy Tales

Neo-Royalism: Government for sale

How to Invest: Regime Change

Chinese Tech Supremacy: Holy Crap!

1. Rupture, what Rupture?

Not that there was any doubt about who really “won” Davos, but nearly two weeks’ after Mark Carney’s powerful speech, the whole world is now talking about “rupture” and “middle powers”. Meanwhile Donald Trump continues to react exactly as as you would expect after being upstaged by the Canadian prime minister, unleashing a torrent of Truth Social posts, threatening “Governor Carney” with tariffs, even as US officials conferred with Albertan separatists.

But is Carney right about a “rupture” and the end of the fiction of the rules-based international liberal order? It is a key question for businesses and investors. For all the geopolitical excitement since the start of the year, the reality is that it is hard to see much evidence for it in the economic data or the markets, as Trump himself noted in a triumphalist op-ed in the WSJ.

The S&P500 has hit 52 record highs since Trump’s inauguration, the president crowed. Indeed, it hit another record high last week, surpassing 7,000 for the first time, buoyed by strong earnings growth and expectations for further interest rate cuts. What’s more, the rise so far this year is not being driven by tech stocks, which are below their peaks, but a broader range of sectors, including energy, materials and consumer staples. Every forecaster expects another strong year for stock markets.

US inflation remains low and falling, despite tariffs, while US economic growth in the fourth quarter of last year was remarkably robust. Nor is it just in the US where growth forecasts are being revised upwards. Eurozone growth held up well in 2025, with three of the four largest economies growing faster than expected. Similarly, the UK economy grew by 0.3 percent in the fourth quarter, again beating expectations. Despite grappling with deflation, China is likely to growth at close to 5 percent this year.

Two of the largest middle powers - the European Union and India - last week agreed wha Commission President Ursula von der Leyen called the “mother of all trade deals”. Meanwhile, Sir Keir Starmer became the latest western leader to beat a path to Beijing, seeking to boost trade with China, with Trump to follow in April. Globalisation, it seems, is far from dead; global trade is forecast to grow 2.6 percent this year, having grown 7 percent in 2025.

Even Trump’s tariff threats shouldn’t be taken too seriously, According to a new analysis by Bloomberg, Trump has only followed through on about 27% of tariff threats he’s made since re-election. That might explain why South Korea’s benchmark stock index gained on the day even after Trump said he would raise US tariffs on South Korea. Meanwhile the Supreme Court may yet be about to significantly curtail his tariff-raising powers.

The one place where one can see some evidence of rupture is in the dollar, gold and silver markets, where for much of last week the debasement trade was in full swing. But that abruptly reversed on Friday following news of the nomination of Kevin Warsh as the next Federal Reserve chairman. Silver prices and gold futures had their biggest falls on Friday since 1981. Sentiment was also helped by Treasury Secretary Scott Bessent restating the administration’s support for a strong dollar, following comments by Trump that suggested the opposite. Besides, a weaker dollar, which many economists think justified on valuation grounds, need not mean an end to dollar supremacy.

None of this means that there is no rupture. The economy and markets’s apparent indifference to geopolitical shocks may simply reflect the resilience of supply chains, or the reality that the world is awash with liquidity as a result of loose fiscal and monetary policy, that the AI capital expenditure boom has outweighed other factors, that markets are myopically focused on the very near-term, or that they find it notoriously hard to price tails risks and regime changes.

For reasons that I will explore later in this post, I still believe that we are living through The End of the Economic World as We Knew It. Nonetheless, it is important to recognise that as things stand, Trump is entitled to his victory lap, while mainstream economics has some explaining to do.

2. Warsh’s Fairy Tale

Kevin Warsh’s nomination as the next Fed chair does seem to have taken one of the biggest risks that was worrying investors off the table. The market seems to have taken his choice of the experienced former Fed governor over “the other Kevin”, White House economic adviser Kevin Hassett, as a sign that central bank’s independence will be maintained. This followed indications that the Supreme Court will further protect its independence by throwing out Trump’s attempt to fire Governor Lisa Cook for an alleged mortgage application violation.

Whether the market is right be so confidence in Warsh remains to be seen. An impressive array of serious figures across the markets and economic policy-making world have testified to his suitability. Indeed, support from Wall Street appears to have been crucial in securing him job, according to the WSJ. Perhaps the rest of us should simply their word for it rather than paying attention to some of the nonsense that he talked when campaigning for the job over the last year.

In public, at least, Warsh certainly seems to undergone quite a transformation. He made his name as an inflation hawk and critic of QE in 2010, over a decade before the slightest sign of inflation appeared on the economic horizon. He has since switched to becoming an ardent advocate of lower interest rates, even as inflation remained well above the Fed’s 2 percent target, thereby endearing himself to President Trump. His argument is that the US is on the brink of AI-driven productivity boom and can thus grow robustly without inflation.

Whether he can actually deliver lower interest rates will depend on whether he can convinced the rest of the Fed committee to follow his lead, given that his would be just one vote among 12. That in turn will depend upon whether he can deploy convincing arguments. Most of them, including the Fed staff, tend to think of inflation as being driven by the amount of slack in the economy. But as Greg Ip wryly notes in the WSJ, while Warsh regularly disparages such models, his own explanations for inflation are “eclectic”, at times drawing on commodity and stock prices, the money supply, productivity and federal spending.

Alongside his fixation with the need for lower interest rates, Warsh appears to have convinced himself that the size of the Fed’s balance sheet somehow lies at the heart of America’s economic problems, favouring Wall Street over Main Street. He appears to believe that the Fed could shrink its balance sheet by selling assets and reducing bank reserves without pushing up bond yields or causing a bank funding crisis that could squeeze the supply of credit. William Dudley, the former head of the New York Fed, argued in a column for Bloomberg last year - convincingly in my view - that this is “mostly a fairy tale”.

That said, there is no question that role of the Fed and central banks in general is overdue some fresh thinking. There is no question that QE failed to work as intended: as Dudley notes, substituting the world’s most liquid access (cash) for the world’s most second liquid (Treasuries), failed to produce much stimulus. At the same time, it carried substantial societal costs, taking central banks into distributional territory that should be the prerogative of fiscal authorities. One question that Warsh and other critics of QE have not fully answered is what would they do differently if confronted by a similar crisis?

Meanwhile the real test of the Fed’s independence will come if and when inflation rises. Will Warsh, like Jay Powell, the current chairman, be willing to risk the ire of the president and withstand his inevitable bullying? If he’s wrong on his productivity hunch, the test could come sooner than he thinks.

3. Government for Sale

One of the ways in which we are surely living through a rupture is in the way that the Trump administration’s approach to governance at both a domestic and international level. Amid strong competition, one of the more astonishing stories to emerge so far this year is news that four days before Trump’s inauguration last January, lieutenants to an Abu Dhabi royal secretly signed a deal with the Trump family to purchase a 49% stake in their fledgling cryptocurrency venture for half a billion dollars. According to the WSJ:

The buyers would pay half up front, steering $187 million to Trump family entities… The investment was backed by Sheikh Tahnoon bin Zayed Al Nahyan, an Abu Dhabi royal who has been pushing the U.S. for access to tightly guarded artificial intelligence chips, according to people familiar with the matter. Tahnoon—sometimes referred to as the “spy sheikh”—is brother to the United Arab Emirates’ president, the government’s national security adviser, as well as the leader of the oil-rich country’s largest wealth fund.

Under the Biden administration, Tahnoon’s efforts to get AI hardware had been largely stymied over fears that the sensitive technology could be diverted to China… Trump’s election reopened the door for him. In the months that followed, Tahnoon met multiple times with Trump, Witkoff and other U.S. officials, including in a March visit to the White House... Two months after the March meeting, the administration committed to give the tiny Gulf monarchy access to around 500,000 of the most advanced AI chips a year—enough to build one of the world’s biggest AI data center clusters.

The White House insists that Trump was not involved in the investment and that there is no conflict of interest. But one legal expert quoted by the WSJ reckons that the transaction looks like a violation of the foreign emoluments clause, designed to prevent any government official from being in the pocket of a foreign government, “and more to the point, it looks like a bribe”. The transaction “should be a five-alarm fire about the federal government being for sale.”

Indeed, the Abu Dhabi story looks like the latest evidence of what Stacie Goddard and Abraham Newman and have described as Trump’s “neoroyalist” approach to international politics, more akin to a 16th century monarchy, under which foreign policy has become a tool to channel money and status to the president and his closest associates. As they explained in the New York Times:

National interests are eclipsed by those of elites. Rather than compete with rivals, Mr. Trump is willing to collude with them in order to advance his court’s parochial interests…

As one distinguished British international relations expert points out to me, the neoroyalist label is not quite right. The early modern European royal families, such as the Tudors or Hapsburgs, were sophisticated dynastic marriage-makers, which was the diplomatic instrument of the time, whereas Trump appears to be motivated simply by making money for himself and his clique, or what might he more accurately refers to as “The Syndicate”. Newman and Goddard again:

Mr. Trump’s clique also centers on his family members and individuals who donated to his 2024 campaign (like Elon Musk and Paul Singer, the billionaire founder and co-chief executive of the hedge fund Elliott Investment Management). Ukraine peace negotiations continue to be led by Mr. Trump’s fellow real estate magnate Steve Witkoff and Mr. Trump’s son-in-law Jared Kushner.

While Mr. Trump boasts that the Venezuela intervention will increase American prosperity, there is actually little promise of national benefit. Instead, the gains appear to be flowing to Mr. Trump and his insiders. Amber Energy, an affiliate of Mr. Singer’s hedge-fund company, won an auction for Citgo, the U.S. subsidiary of the Venezuelan state-owned oil company, a few months ago and is now strategically positioned to play a key role in refining and distributing that oil.

Mr. Trump’s trade policy follows a similar script. While not delivering a rebirth in U.S. manufacturing jobs, tariffs have served as a ready-made tool to get countries and companies to tithe. South Korea and Japan have collectively pledged hundreds of billions in investment funds operated under opaque governance rules. Vietnam fast-tracked the approval of a $1.5 billion Trump family golf course at the same time that it sought to reduce its tariff rate.

One might also add that the person who is reported to have put the idea of annexing Greenland into Trump’s head was Ronald Lauder, the billionaire heir to the Estee Lauder fortune and Trump donor who has mining interests on the island. Lauder, who also has extensive connections at the highest levels of the Kremlin, was also the first person to receive a contract under Trump’s Ukraine minerals deal. It is surely purely coincidental that Lauder also happens to be the father-in-law of Kevin Warsh, Trump’s pick to be the next Fed chairman.

If Goddard and Newman’s thesis is right - and it is hard to believe it is not when the Trump family has reportedly increased its personal wealth by at least $4 billion since the election - then it is hard to argue with their conclusion, which happens to chime with Mark Carney’s warning:

If other countries do not act quickly to check Mr. Trump’s impulses, they are likely to enable a global order based on extraction and dominance.

4. Regime Change

If we are witnessing a rupture rather than a transition in the global order, then the implications for investors are potentially far-reaching, no matter how benign the immediate outlook for the global economy and markets. As David Bowers of Absolute Capital Research said in a note to clients last week:

Business models, financial structures and asset classes that thrived under rules-based globalisation are about to have the rug pulled out from under them…

This new regime shouldn’t be seen as a risk to hedge but rather something to position for... The Trumpian model isn’t “just” about tariffs, it is potentially far more revolutionary than just that.

Among the consequences that investors need to consider, Bowers highlights:

a world that is moving away from a rules-based, efficiency-maximising model to a geopolitically fragmented, security-first system will be one in which there is much greater regional and country dispersion of outcomes

a world that is shifting away from globalisation is one in which one can expect structurally higher and more volatile inflation

expect to see more state intervention in capital allocation and national savings to be harnessed to provide anchor capital alongside hyperactive industrial policies. Expect foreign capital to be screened and to become more politicised

a word in which national security and geopolitics - rather than efficiency - become the organising principles for capital formation will require new benchmarks. Passive investing that follows the world as it is today will be no use in navigating these new realities

a world of weaponised strategic autonomy will bring new investing themes to the fore. Sectors such as energy, food, critical minerals, defence and real assets should do well; but investors may demand a higher risk premium for businesses exposed to China or with long cross-border supply chains

Of course, all this begs the question of what will become of Europe in a new neoroyalist world order - a core theme of Wealth of Nations since it launched. So far there is little evidence of it being prepared to make the bold strategic choices necessary to become a carnivore in a world of herbivores (see Europe’s Century of Humiliation?). A test of seriousness would be the launch of a big joint borrowing programme to fund common defence. As Carney warned, countries that are not at the table are on the menu.

5. Chinese Tech Supremacy

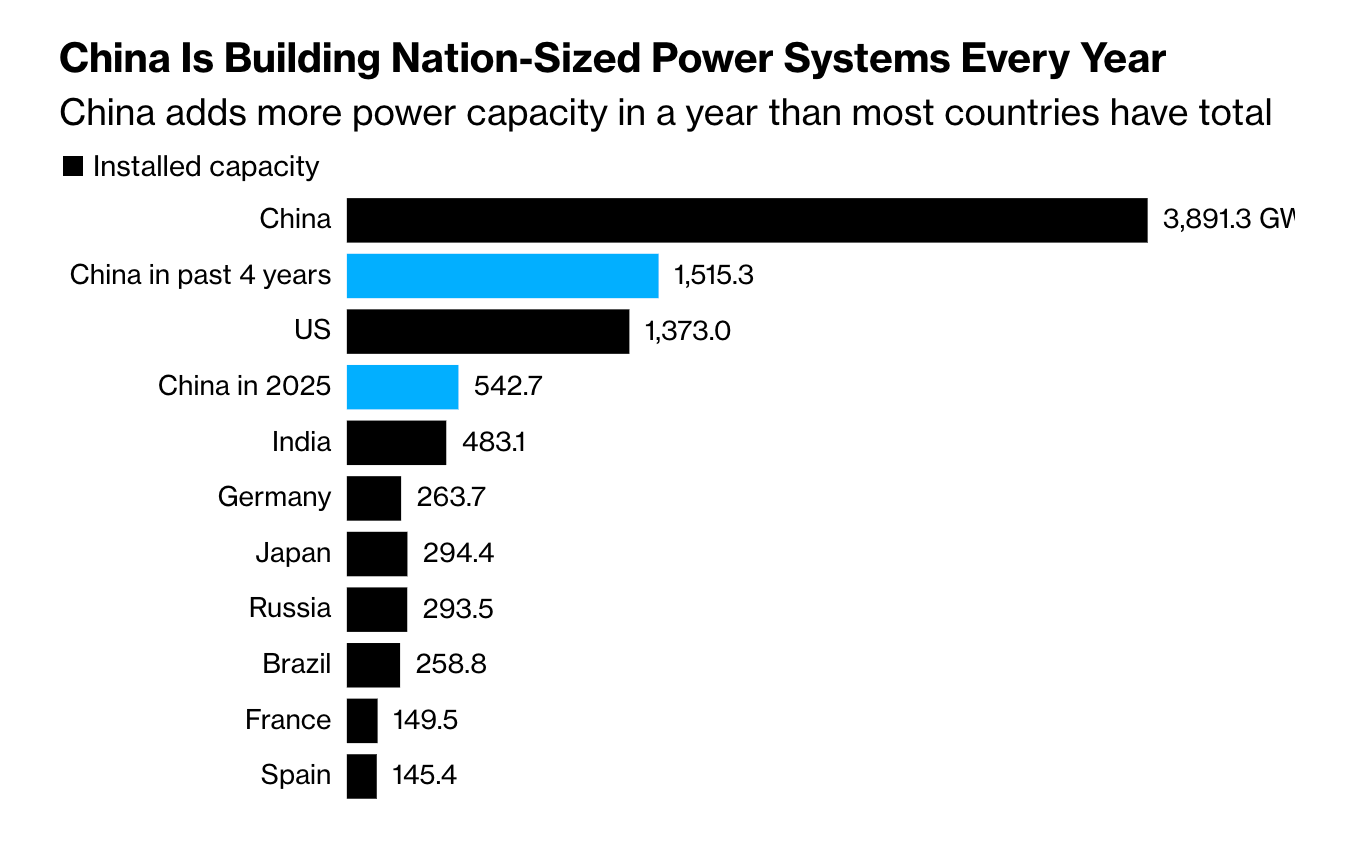

Of course, part of what lies behind this rupture in the global order is the astonishing rise of China and its global leadership in new technologies. Two items caught my eye this week that illustrate the sheer scale of this revolution.

The first was this chart from Bloomberg which shows how China is undertaking an energy-building boom unlike anything the world has ever seen. It added 543 gigawatts of new capacity across all technologies last year, according to data from the National Energy Administration on Wednesday. That’s 12% more than all the power plants combined in India as of the end of 2024. The generation China has added since the end of 2021 is also larger than the entire US system.

China’s abundant electricity supply, with most of the new generation coming from renewables, gives it a potentially significant advantage over America in the intensifying tech race as Trump doubles down on 20th century fossil fuels and US electricity prices soar (see Electric Shock and Chinese Power).

The second was this piece by Joanna Stern, the WSJ’s tech columnist, headlined: I Test Drove a Chinese EV. Now I Don’t Want to Buy American Cars Anymore. Stern writes:

My time with the car confirmed what experts in the auto industry have long been saying: Holy crap, China is winning the digitally enhanced electric-car race.

Chinese EV makers such as Xiaomi, BYD and Geely have earned global accolades because their cars deliver longer battery ranges and deeply integrated digital platforms. We’re talking software that feels smooth like a brand new smartphone, not a screen you have to jab five times to load a map. Plus, they often cost tens of thousands of dollars less than Western competitors. In Europe and Mexico, they’re blowing past Tesla and other EV rivals.

The SU7 Max feels exactly like what you’d expect from a tech company making a car, not a car company making tech.

Indeed, this breathless tribute to Chinese tech comes as EV sales in Europe last month surpassed those of petrol-powered cars for the first time, rising to 22.6 percent of all sales. Meanwhile sales of hybrids easily topped them both. It also comes as the US has abolished subsidies for EVs and Europe is pushing back deadlines for phasing out internal combustion engines. The challenge facing US and European carmakers, as in other tech sectors, is not that Chinese manufacturers are subsidised, but that their kit is simply better.

Not sure why appointment of Kevin Warsh should have led to a reversal of the secular debasement trade trend insofar that he wants to lower US interest rates, which should all other things being equal, tend to lower the dollar?

On a different note, the EU-India trade agreement puts Starmer's apparent preference for single market alignment rather than rejoining the CU into sharper focus, underlining the puny benefits of UK trade independence relative to trade frictions with our neighbours.

A quick aside on the Alberta canoodling. As ever with Chump you can play his own game back to him - I think most of the coastal US states would be up for jumping ship to Canada if this sh!tshow doesn't get checked eventually or something really egregious happens such as a blatant attempt to rig the midterms.

I'd love to see the reaction if Carney floated that...!!