The War on Big Tech

The War on Big Tech

What caught my eye this week including volatile stocks, Britain's block hole, how to defeat the far right, the trouble with Elon Musk, busting Google's monopoly and France after the Olympics

1. Stock market

So is that it? Is the summer stock market panic over? After a 12 per cent fall in the Nikkei 225 index on Monday, its biggest one day fall since Black Monday in 1987, there was feverish talk of a full blown global market meltdown. Yet by the end of the week, the Nikkei had recovered half of its losses while the S&P500 index of leading US shares ended up 3.5 per cent higher than where it had started.

What happens to the market from here doesn’t just matter for investors. It is a political issue too. Donald Trump was quick to jump on the sell-off last week calling it the “Kamala Crash”. As many US pundits noted last week, if there is one thing that is sure to derail the revival of Democrat fortunes since they swapped Joe Biden for Kamala Harris at the top of the ticket, it would be a stock market crash and recession.

Fortunately, it now seems clear that what fuelled the crash was not in fact recession fears, which as I noted last week, always seemed overblown. The trigger was last week’s unexpected rise in Japanese interest rates. That caught out hedge funds which had been borrowing in Yen to invest in foreign markets. It didn’t help that the unwinding of this Yen “carry trade” came just as investors were starting to question the hype around AI, which had been triggering sharp falls in tech stocks too. Indeed, some of this cheap Yen borrowing may have been used to buy tech shares.

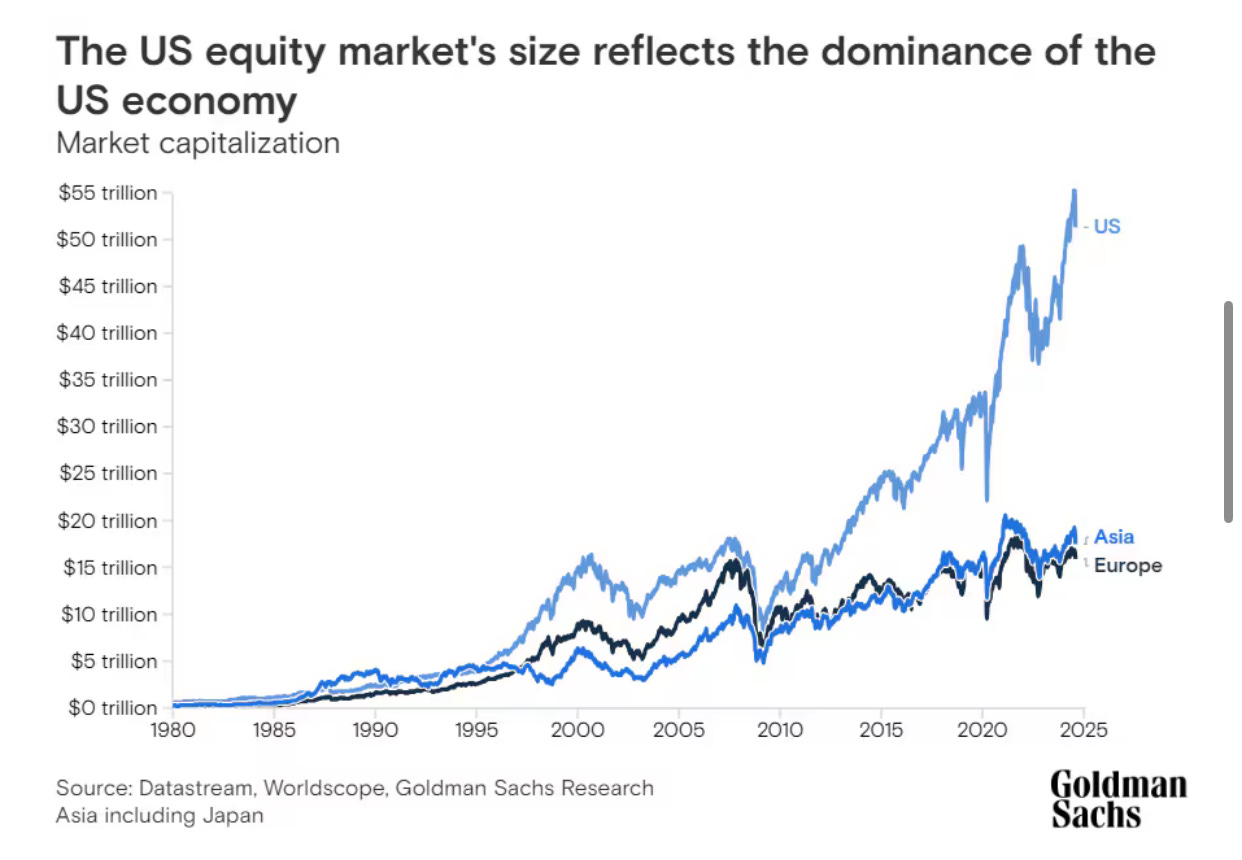

Even so, the US stock market may still be vulnerable between now and polling day. The S&P500 trades at an eye-watering 33 times next year’s forecast earnings, the highest multiple for all but three of the last 150 years. This chart from Goldman Sachs shows just how extraordinary has been the rise in US stocks in recent years, far surpassing all other markets.

According to Peter Oppenheimer, the investment bank’s chief strategist, those valuations aren’t necessarily a sign of irrational exuberance. US companies have seen much more profit growth than their counterparts in the rest of the world. He doesn’t anticipate a bear market because he doesn’t expect earnings to fall, not least because the Fed has plenty of scope to cut interest rates to prevent a recession. But he does note that the valuations do imply “that the advantage in the US will continue in the future, but that isn't necessarily clear.” He recommends diversifying.

An alternative strategy is to take a leaf out of Warren Buffett’s playbook. This week Berkshire Hathaway, the investment vehicle that he has run for six decades, has cut its stake in Apple by almost half, to $84 billion and increased its holdings of cash and Treasury bills increased from $189 billion in the first quarter of the year to $277 billion at the end of June. Why would he sit on such a vast cash pile? According to The Economist, one reason is that “he sees few cheap, high-quality companies in which to invest. The stockmarket is expensive across the board”.

That sets up what may be a nervous few months ahead of the US election. All eyes will be on the Federal Reserve. The markets have already successfully bullied the Bank of Japan into rowing back on its commitment to keep raising interest rates. Can they now bully the Fed into a half a percentage point interest rate at its next meeting in September, as many say is necessary to stop the economy sliding into recession? More than the fate of the S&P500 may be riding on the answer.

2. Labour’s Black Hole

Amid the focus on the US stock market, spare a thought for London which just can’t seem to get a break. As I’ve previously noted, it trades at just half the multiple of the US market and 20 per cent discount to European markets. Yet this did not protect it from a being sold-off in the recent turmoil. Instead, the FTSE100 is back where it was at the beginning of May. Meanwhile the consequences of this persistent low valuation continue to unfold. London has lost its historic status as home to the global mining sector to Sydney and Toronto; and TP-Icap, the brokerage, says that it is considering listing its data arm in New York in what would be another blow for the City.

This stock market underperformance is another thing for Rachel Reeves to worry about as she tries to figure out how to fill a black hole in the public finances left by the Tories. Low valuations means a high cost of capital. Not helpful for a chancellor and government whose primary mission is to restore economic growth by means of higher private investment in infrastructure. Reeves has already said that taxes will have to rise, but having pledged not to raise the rate of income tax, national insurance, VAT and corporation tax, she doesn’t have many options. Yet that mostly leaves taxes on wealth which could have a negative effect on capital.

No wonder Reeves is reported to be considering changes to the fiscal rules to create more scope for increased borrowing, despite having pledged to stick by the previous government’s fiscal rules. There is speculation that she will change the way that public debt is measured to exclude the losses accumulated on the Bank of England’s vast holdings of government bonds acquired under its quantitative easing programme. That could treble the amount of fiscal headroom to around £26 billion against her target that debt must be falling as a percentage of GDP after five years.

To abandon yet another pre-election pledge so quickly, having previously also ruled out tax rises, will inevitably expose Reeves to further accusations of bad faith. But the chancellor would be following in a long tradition of junking fiscal rules as soon as they become inconvenient: Britain has had nine sets of fiscal rules since the global financial crisis, changing its rules more frequently than any other country. Nor is Reeves likely to suffer much pushback from economists or the markets for this accounting fiddle. Everyone agrees that the rules are poorly-framed, not least because they make no distinction between borrowing for spending and investment.

Reeve’s real problem is that while this ruse might buy her some breathing space, it makes no difference to public debt over the longer-term. As the IFS points out, the losses on the Bank of England’s bond holdings will crystallise sooner or later when the bonds are sold or redeemed. Critics will rightly say that if the change in accounting treatment makes no difference to long-term debt, how can it be a credible basis upon which to base an increase in public spending?

A better approach would be to introduce a new target based on net worth, as I discussed in this post. This is a measure of debt that includes all liabilities, including the vast unfunded public sector pension obligations that the current measure ignores, minus the value of public assets. This has the advantage of focusing attention where it should be - on Britain’s decades of woeful under-investment. Indeed, the UK’s net worth is currently an astonishing minus 60 per cent of GDP, the second worst of any major economy after Italy, according to the International Monetary Fund.

For years, the British state has been consuming national wealth rather than creating it, resulting in vast hidden debts that will be passed onto future generations. If Labour is serious about reversing this dismal legacy, it should adopt a target that incentivises investment over spending. That will justify higher borrowing, but only if it rebuilds net worth. Reeves has previously hinted at such an approach. Time to bite the bullet.

3. Far right

Of course, Reeves will also be crossing her fingers that the horrendous far right riots across Britain last week do not further damage the country’s reputation among investors. To what extent the riots contributed to the last week’s fall in sterling against the dollar is unclear. The pound has now fallen for four straight weeks from its July 17 high of $1.30, primarily driven by expectations of quicker interest rate cuts. But it is striking that the sterling rallied on Friday when it appeared the riots were under control. Most analysts remain bullish on the pound: Goldman has raised its target value to $1.32, though still below its pre-Brexit level of $1.45.

Nonetheless, there is clearly a risk that a failure to stamp out the violence could tarnish Sir Keir Starmer’s premiership and undermine global investor confidence in the post-election narrative that Britain had left behind the chaos of the Tory years. ReutersBreakingviews raises the spectre of the gilets jaunes protests that exploded in France early in Emmanuel Macron’s presidency from which his popularity has never recovered, noting that he still has less than a 30 per cent approval rating. Yet it also acknowledges that there is some way to go before we reach that point:

Starmer does have a considerable stash of political capital following his Labour Party’s landslide victory in the July 4 election. And for now, business seems relaxed. Representatives of large multinationals have told Breakingviews they still think the UK is a safer bet than countries like Germany and France where far-right parties with more radical policies around immigration pose more of a threat to economic stability.

In fact, on the assumption that the violence is over, I think Starmer emerges from this early test of his leadership rather well. The prime minister called out the violence for what it was - far right thuggery - and galvanised the criminal justice system into swift and exemplary harsh treatment of the rioters.

It is his opponents on the right, both in politics and the media, who have been shamed by the violence, not least by their initial attempts to make excuses for the rioters by suggesting they were expressing legitimate grievances over immigration or by peddling ludicrous myths about “two tier policing”. The initial silence of the six candidates for the Conservative party leadership even as their party’s own “stop the boats” election slogan features prominently at the far right demonstrations spoke volumes about the state of that party. But the fact that by the end of the week all the right-wing papers were condemning the rioters without equivocation and celebrating anti-fascist counter-protests suggests that a corner may have been turned.

Of course, once the violence is over and the thugs banged up, attention will have to switch to addressing the underlying causes of this surge in support for the far right which surely lie in the dire poverty and lack of opportunity in far too much of Britain, in part reflecting the mismanagement of the economy over the past 14 years and failed Tory promises of Brexit and “levelling up”. A compelling analysis of what it will take to see off the far right was offered by Margaret Hodge in the Economist. The former Labour MP was faced with a huge rise in support for the far right British National Party in her constituency of Barking between 2000 and 2010 which she confronted through the simple expedient of focusing relentlessly on solving local problems:

We had to fundamentally change the way we did politics. We started on the basis that, as Tip O’Neill, a former speaker of America’s House of Representatives, once put it, “all politics is local”.

To reconnect with people, we started with what mattered to them. People’s concerns come from their immediate environment, whether that relates to local issues, from car parking to rubbish tips, or national issues that affect them locally, such as the lack of housing or immigration. They don’t want to hear about the latest obsession in the Westminster bubble unless it has a direct impact on them.

So we wrote directly to voters, inviting them to coffee afternoons and street meetings. We listened to them in these settings and let them set the agenda. Usually, there was something we could do about the local issues raised, so having listened we would act on their concerns.

Then I would write to them individually again, telling them what we had done.

As an addendum, it is striking that the young Labour party staffer who played a key role in delivering this strategy to see off the BNP threat in Barking was Morgan McSweeney, who is now Sir Keir Starmer’s closest aide and the architect of Labour’s political strategy which delivered the party’s landslide election victory. Indeed, as this superb profile of him published earlier this year shows, what McSweeney learned in Barking was to become central to the entire Starmer project.

4. Elon Musk

Meanwhile the other focus of political attention post the far right riots has been on the role of social media, whether that be in spreading disinformation, contributing to the radicalisation of the thugs, or enabling them to organise and coordinate their activities. Particular attention has been focused on X, as I still can’t get used to calling the social media platform previously known as Twitter, and its owner, Elon Musk, who has taken to reposting far right accounts, pushing far right narratives and launching extraordinary attacks on Britain and Starmer. There have been calls for tougher laws to crack down on social media sites.

I am certainly not going to defend Musk, who is emerging as an increasingly sinister figure in politics on both sides of the Atlantic. For example, this piece in the Washington Post suggests there is credible evidence to believe that Musk’s X is deliberately suppressing accounts that support Kamala Harris in the US presidential election. But I would also note that in pushing his own agenda, Musk is behaving no differently to any other billionaire media owner, except that he is doing it openly, rather than hiding behind editors. It is also worth noting, as Professor Julian Petley of Brunel University explains in this piece for Byline Times, that the reason Britain does not have tougher rules on harmful online speech is because the newspapers themselves lobbied against them, on the not unreasonable grounds that they would infringe on free speech and make the press liable for the comments of their readers.

But for an alternative view on the role of social media, I do recommend listening to this podcast featuring Sir Nick Clegg, the former British deputy prime minister, being interviewed by Alasdair Campbell and Rory Stewart. Clegg is now the global head of public affairs for Meta, which owns Facebook and other social media platforms, so anything he says needs to be heard in that context. I should also note that the interview was recorded long before the far right riots. Nonetheless, Clegg puts up a spirited defence of social media and makes some interesting points:

Clegg notes that Meta spends hundreds of billions of dollars a year on content moderation, employing armies of people around the world as well as AI to remove harmful or illegal content. He is also amusing on some of the difficulties this can present when trying to create standards that can apply globally. For example, some Scandinavians like to share pictures of themselves naked in the sauna and get upset when their posts are taken down because of more prudish attitudes towards nudity in the rest of the world. Clearly X has been applying very different standards of content moderation since Musk took over and it may be that the cost of having to police content to meet new UK standards under the new Online Safety Act explains some of his hostility towards Britain.

Clegg also insists that there is no research anywhere in the world to suggest that social media can lead to increased political polarisation. Campbell and Stewart consider this highly unlikely, though I note that they have not published any links to studies that might suggest Clegg is wrong. I was not able to find any studies to contradict Clegg with a quick Google search but was able quickly to find several that backed up his assertion. In any case, I don’t find his claim so implausible. After all, there were pogroms of the sort that the far right thugs attempted when they set fire to a refugee hostel in Hartlepool last week long before there was social media. Right-wing British newspapers have been pushing Islamophobic, race-baiting tropes for years without any help from social media. Indeed, the Daily Mail’s history of support for fascism is a matter of public shame.

Clegg also points out the extent to which social media has been a global force for good. I agree. One of the benefits of social media is that it allows anyone to call out disinformation, hold the powerful to account and challenge narratives. Anyone could go online and call out Musk’s offensive posts and many did. Compare that to old media, where there is often no recourse to challenge poor reporting. The Times, for example, seems to have adopted a new policy of shutting down comments on any story where readers might call into question the editor’s judgment and instincts. As Clegg says, who wants to go back to a world where newspaper editors get to dictate what you are allowed to know?

More importantly, social media plays a vital role in spreading and promoting democracy. Contrary to the conventional wisdom in January, this is turning out to be a very bad year for authoritarians and the far right around the world, thanks in part to the role of social media in circumventing official media. Social media played a role in the ousting this week of Sheikh Hasina, Bangladesh’s authoritarian prime minister, after weeks of protests. And it was social media that enabled the Venezuelan opposition to alert the world to the crass attempts by Nicolas Maduro to steal last month’s election, and thanks to social media pressure on governments in the rest of South America that Maduro’s days may yet be numbered. It comes as no surprise that Maduro is following in the path of many authoritarians in now blocking access to X and WhatsApp.

Clegg is a thoughtful man who has had a fascinating career in EU politics in Brussels, Westminster politics and now Silicon Valley. For anyone interested in contemporary British history, the whole two-part interview is well worth a listen.

5. Google antitrust

It is not just in Britain that Big Tech is under assault. For similar reasons but by different means, it is under attack in the US too. In America, the weapon of choice is not online safety rules but antitrust law. In a landmark ruling this week, a Federal judge found Google guilty of abusing its market power to kneecap competition in web search by hammering out restrictive contracts with Apple and other phone makers that required them to install Google as the default search engine.

“Google is a monopolist, and it has acted as one to maintain its monopoly,” Judge Amit P. Mehta of the U.S. District Court for the District of Columbia wrote in his judgment on Monday.

The details of this case are less important than what it says about the direction of US attitudes towards entrenched corporate power. At this stage, it is far from clear what remedies Google might be required to apply to address is anti-competitive behaviour, or even whether the case will get that far, given that Google will appeal. But the fact that a court has found against Google is a huge victory for what has become known as the New Brandeis movement in American legal circles that has been gaining power and influence for several years and two of whose leading exponents - Lina Khan and Jonathan Kanter - are now ensconced as the two top trade officials in the Biden administration as head of the Federal Trade Commission and head of the Department of Justice’s antitrust division respectively.

The background and origins to the new Brandeis movement was brilliantly explained in this 2021 essay in the Wall Street Journal. It is named after Louis Brandies, the Progressive Era crusader turned Supreme Court justice, who led many of the legal assaults on the monopolistic “trusts” around the turn of the 19th century, not least J.P Morgan’s attempt to consolidate the New England railways. As the WSJ notes, Brandeis’s approach to antitrust rested on two core themes:

“First, that the purpose is more about preserving democracy than fostering growth… Second, as he argued in his 1934 book, “The Curse of Bigness,” big business is suspicious in itself, whether economic harm can be proven or not.”

But by the 1980s, Brandeis’s ideas had fallen out of favour. His intellectual nemesis was a Yale law school professor, Robert Bork. He argued that the Brandeisian crusade against bigness had gone too far. “The only legitimate goal of American antitrust law,” he declared, “is the maximization of consumer welfare.”

Bork’s basic view was that antitrust should focus on economics and shed political and social aims. He coupled that framework with a belief in the superior wisdom of the private sector over the public. Attempts by business to gain damaging monopoly power would inevitably be corrected by free markets, he argued, while government intervention to fix perceived problems would cause lasting harm.

This view has effectively held sway in the US political legal system for four decades - until now. The emergence of the New Brandeis movement represents a paradigm shift in US politics. Much of what animates it is the rise of big tech. Apart from the case against Google, the Biden administration is pursuing cases against Amazon and Meta and is seeking to block Microsoft’s $69 billion acquisition of gaming company Activision Blizzard and is investigating Microsoft’s investment in OpenAI. From the WSJ again:

[The New Brandeis] advocates believe that the dominant, winner-take-all platforms of Google, Amazon, Facebook and Apple are reminiscent of the interlocking, network-like behemoths that fostered the original antitrust movement: the railroads, the banks, Standard Oil and U.S. Steel. To Ms. Khan and her colleagues, the threat posed by the new giants requires dusting off old trust-busting strategies. If the neo-Brandeisians get their way, the federal government would challenge more mergers and business tactics and break up more companies.

But the shift is about more than big tech and tougher enforcement. It’s about a change in the underlying philosophy of how Washington has governed corporate America since the 1980s. The new framework is more rooted in social and political goals than economic ones; more focused on the size of companies per se, less on trying to assess whether that size is good or bad for the economy; and more sympathetic to suppliers, small business and workers, even at the expense of consumers.

But while the New Brandeis movement was winning adherents in the White House and Congress, the big question has been whether it could win in the courts, where much of the judiciary is steeped in Borkian orthodoxy. The Google case would appear to suggest that the answer is that the tide there too may be shifting, much to the frustration of many traditional conservatives. In an editorial this week, the WSJ complained that Google’s monopoly is the result of billions of dollars of investment in building a superior search engine and that phone users are free to switch to an alternative if they want to, so no harm is done. In true Borkian spirit, it noted that:

Antitrust law isn’t intended to punish companies that win in the marketplace. The law is supposed to protect consumers from a monopolist that uses its power to raise prices or restrict choices.

The counter argument can be found in recent Substack posts by Robert Reich, Professor of Public Policy at the University of Berkeley and a former Labour secretary in the Clinton administration. In true Brandeisian style, he argues that entrenched corporate power lies behind much of the disaffection that is giving rise to populism and support for Donald Trump.

Over the last 40 years, the “free market” has been rigged and power has shifted upward to corporate executives and investors who engage in organized bribery — bankrolling lawmakers who change laws and regulations to their benefit.

This has allowed the powerful to monopolize industries, bash unions, pay lower taxes, make big financial bets on Wall Street and get bailed out when the bets go sour, outsource jobs abroad, and pretend they’re job creators who deserve all this power.

The result? The richest 1 percent of Americans now own nearly as much wealth as the bottom 90 percent put together.

In a previous post welcoming the Google antitrust decision, he noted that some of the Democratic party’s biggest donors, including Reid Hoffman, the billionaire co-founder of LinkedIn, and Barry Diller, the chairman of IAC and Expedia, were publicly lobbying Kamala Harris to dump Lina Khan as head of the Federal Trade Commission if she wins the election:

Here’s what I recommend Harris do: Openly tell Hoffman and Diller she thinks Khan is doing a great job and wants her to stay at the FTC — and if they don’t like it, they can keep their money.

With this one gesture, Harris would shut the door to billionaire quid pro quos and demonstrate her independence from Big Tech’s big money.

Can Harris afford to do this? I think so, especially given her surge of support from small donors. If she did this, I suspect her small-donor support would explode even more.

It would also be good for America if Harris shut this door. Big money, especially from Big Tech, is the second-biggest threat to American democracy — after Donald Trump.

As I say, the same fight as in Britain, but fought by different means. The war against big tech may be one of the most consequential ideological battles of our times.

6. Olympic Joy

What a carnival of joy the Paris Olympics has proved to be. Even from an armchair in London, the excitement and exhilaration of the past two weeks has been obvious and infectious. The Games has been staged with such Gallic flair, showcasing the world’s most beautiful City to great effect and with some wonderful touches, including the ringing of the Olympic bell by the winner of each athletics final. For the French themselves, the Olympics seem to have provided a two-week holiday from the deep political divisions following the European and parliamentary elections, providing a rare moment of national unity. No wonder Le Monde asks, will it hold?

Is this just a cheerful and light-hearted intermission? Is it a breath of fresh air after weeks of breath-holding over politics, in a divided country plagued by doubt and controversy? Or is it the sign of a movement revealing more positive trends in French society?

Come Monday morning, reality will once again intrude on French political life. The urgent task of finding a prime minister and government that can not only gain the confidence of parliament and, more importantly, pass a budget that will tackle France’s large budget deficit and comply with eurozone fiscal rules, will return to the top of the agenda. President Emmanuel Macron will clearly be hoping that the Olympic truce can translate into more constructive political engagement.

Of course, that may be wishful thinking. As Le Monde notes, a similar wave of national unity followed the "Black, Blanc, Beur" ("Black, White, Arab") victory of the French football team in the 1998 World Cup under the captaincy of Zinedine Zidane. Yet the didn’t forestall the march of the far right which went on to reach the second round of the presidential election in 2002 under Jean-Marie Le Pen. Closer to (my) home, there is the precedent of the London Olympics in 2012, for my money the only recent Games that can match the spirit of Paris 2024. Yet within five months, David Cameron had made his fateful Bloomberg speech committing himself to an in-out referendum on European Union membership - and the rest, as they say, is history.

I hope for the sake of all French friends and readers that they do not find themselves looking back on this fortnight in 12 years time as the last time they felt the country was truly united, self-confident and at ease with itself.

The writer wins the buzzword bingo prize for the number of mentions of "FAR RIGHT". Obviously his obsession with this mythical group undermines his analysis of what is happening, which is at best superficial. The only positive is that he didn't blame the riots on Farage but I suspect he was tempted. To suggest that Starmer was the key influence would probably make his mind explode